Results¶

This page separates deterministic synthetic examples from real market-data examples. The plots are committed artifacts generated by the notebook clients, so the documentation build stays deterministic and does not depend on live notebook execution or market-data downloads.

Machine-readable copies of the comparison tables are committed under results/:

results/synthetic_comparison.csvresults/real_data_comparison.csvresults/generated_comparison_summary.csvresults/generated_repeatability_trials.csvresults/real_data_method_comparison.csvresults/larger_real_data_comparison.csvresults/ansatz_comparison.csv

For repeatable synthetic benchmark summaries, regenerate a compact comparison CSV with:

python scripts/generate_comparison_results.py

By default this writes results/generated_comparison_summary.csv with classical baselines, multi-seed quantum summaries, feasibility rates, objectives, risk/return metrics, and runtimes. It also writes results/generated_repeatability_trials.csv with one row per method/seed trial. Use --asset-counts, --seeds, --steps, and --methods to expand or tighten the run.

How to Read the Tables¶

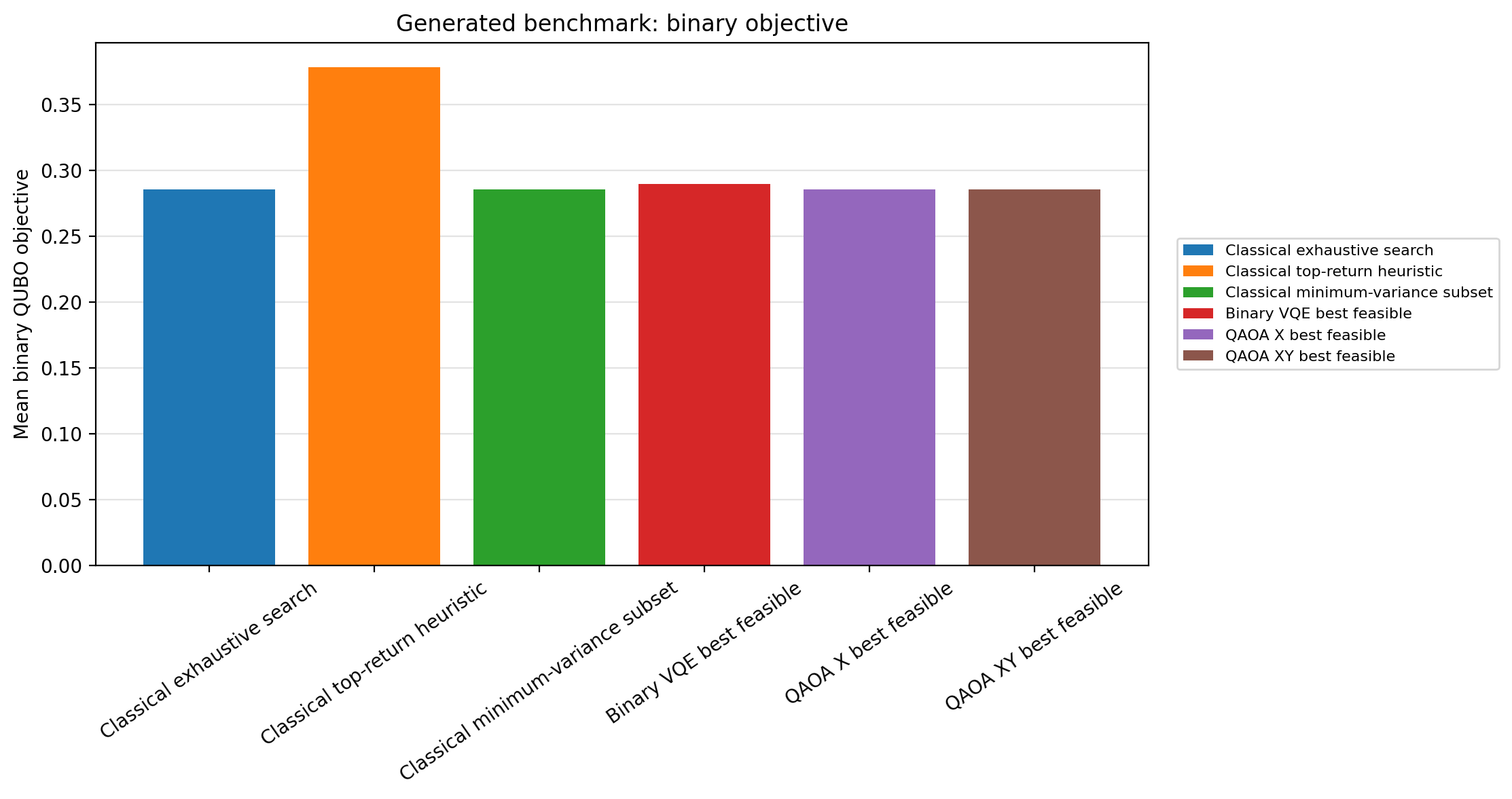

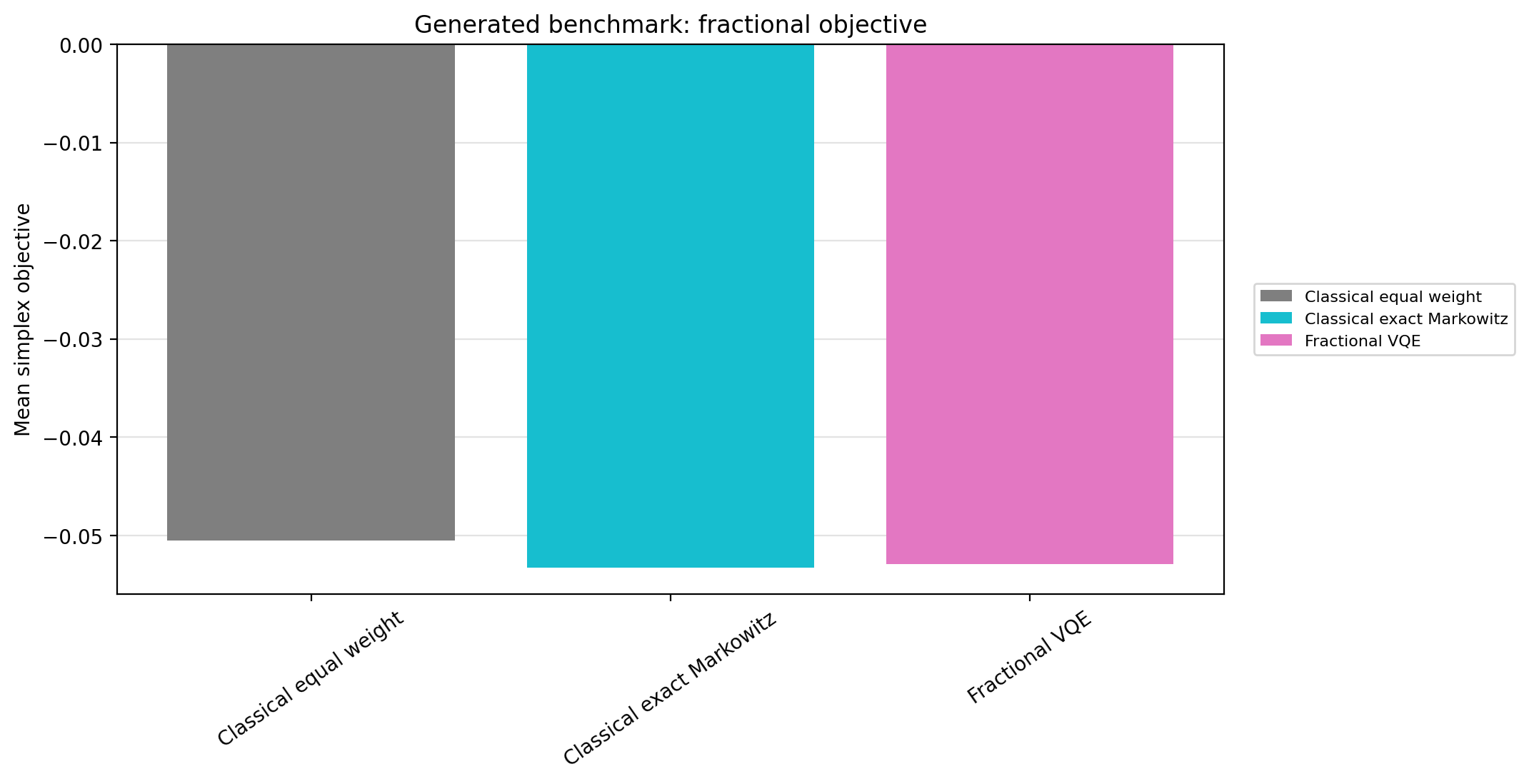

For binary selection methods, lower objective is better for a fixed dataset, risk-aversion value, penalty, and cardinality. For fractional allocation methods, lower simplex objective is better at the same risk-aversion value.

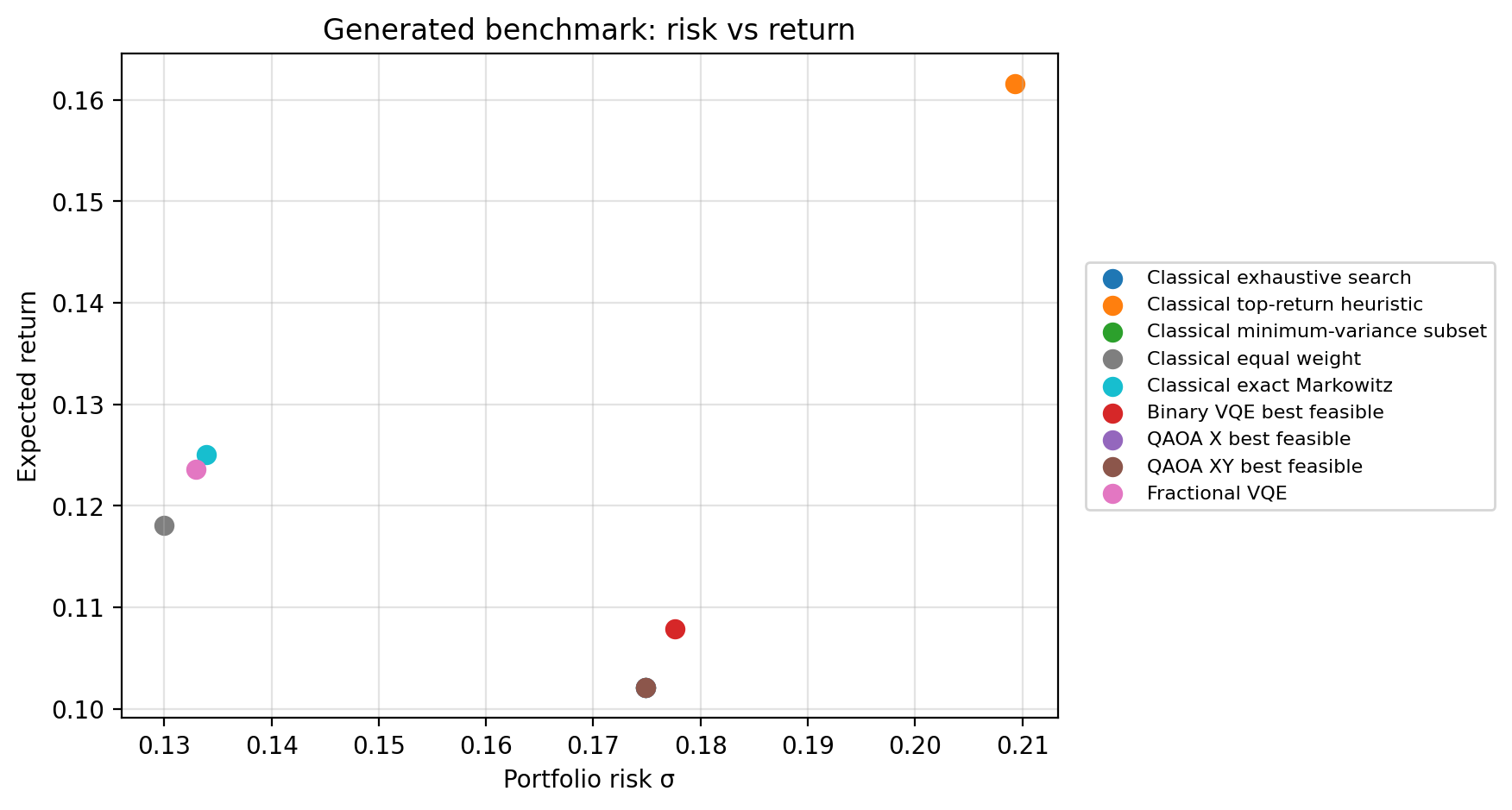

Generated comparison tables include objective_family and reported_weighting columns because binary QUBO objectives and fractional simplex objectives are different mathematical objectives. In generated comparison rows, binary return and risk are reported from equal-weight selected portfolios (x / K) so risk-return plots are comparable with simplex allocations, while the binary objective remains the true QUBO objective evaluated on the raw bitstring x.

The real-data tables report values already saved in notebook outputs. Exact real-data classical optimizer rows should be regenerated together with the market-data notebooks because adjusted prices and shrinkage estimates are provider-dependent.

Synthetic Results¶

Synthetic examples use fixed in-notebook arrays and are therefore the best place for deterministic method-to-baseline comparisons.

Generated Baseline and Repeatability Results¶

The generated comparison files add baseline rows and repeatability summaries from deterministic synthetic data:

Binary baselines: exact exhaustive search, top-return subset, and minimum-variance subset

Continuous baselines: equal-weight allocation and exact long-only Markowitz

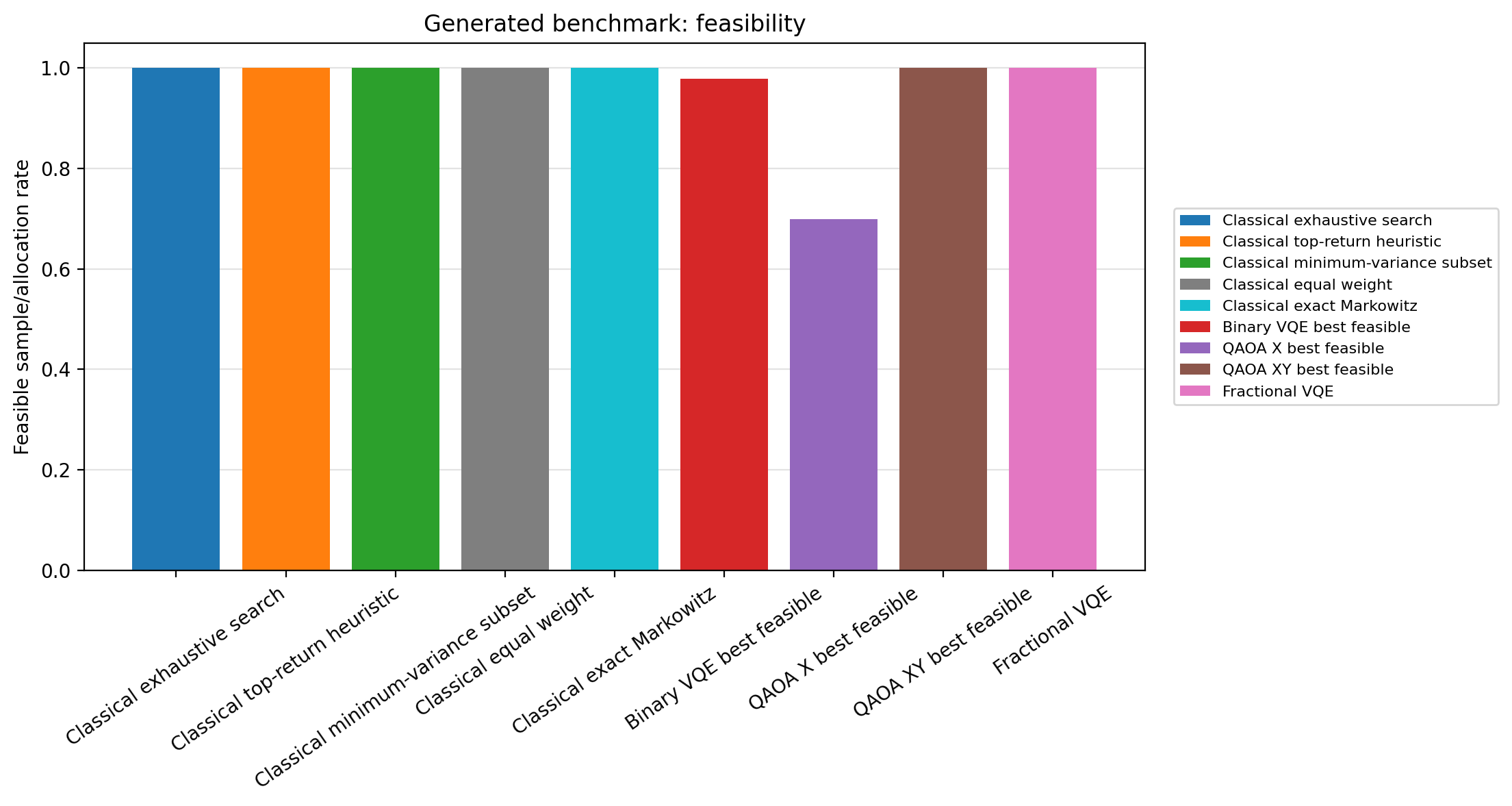

Quantum repeatability: Binary VQE, QAOA X, QAOA XY, and Fractional VQE summarized across seeds, with per-seed rows saved separately

Objective plots are split by objective family so binary QUBO objectives are not visually mixed with fractional simplex objectives

The committed generated CSVs are lightweight benchmark artifacts. Regenerate them after algorithm changes with:

python scripts/generate_comparison_results.py

Dataset |

Method |

Objective family |

Reported weighting |

Seeds |

Mean return |

Mean risk |

Best objective |

Mean objective |

Std objective |

Feasible rate |

|---|---|---|---|---|---|---|---|---|---|---|

Synthetic generated n=4 |

Classical exhaustive search |

binary QUBO |

equal-weight selected |

1 |

0.102055 |

0.174865 |

0.285137 |

0.285137 |

0.000000 |

1.000000 |

Synthetic generated n=4 |

Classical top-return heuristic |

binary QUBO |

equal-weight selected |

1 |

0.161566 |

0.209324 |

0.377932 |

0.377932 |

0.000000 |

1.000000 |

Synthetic generated n=4 |

Classical minimum-variance subset |

binary QUBO |

equal-weight selected |

1 |

0.102055 |

0.174865 |

0.285137 |

0.285137 |

0.000000 |

1.000000 |

Synthetic generated n=4 |

Classical equal weight |

fractional simplex |

simplex weights |

1 |

0.118063 |

0.129968 |

-0.050496 |

-0.050496 |

0.000000 |

1.000000 |

Synthetic generated n=4 |

Classical exact Markowitz |

fractional simplex |

simplex weights |

1 |

0.125046 |

0.133935 |

-0.053292 |

-0.053292 |

0.000000 |

1.000000 |

Synthetic generated n=4 |

Binary VQE best feasible |

binary QUBO |

equal-weight selected |

3 |

0.107872 |

0.177643 |

0.285137 |

0.289414 |

0.006049 |

0.978516 |

Synthetic generated n=4 |

QAOA X best feasible |

binary QUBO |

equal-weight selected |

3 |

0.102055 |

0.174865 |

0.285137 |

0.285137 |

0.000000 |

0.699219 |

Synthetic generated n=4 |

QAOA XY best feasible |

binary QUBO |

equal-weight selected |

3 |

0.102055 |

0.174865 |

0.285137 |

0.285137 |

0.000000 |

1.000000 |

Synthetic generated n=4 |

Fractional VQE |

fractional simplex |

simplex weights |

3 |

0.123596 |

0.132920 |

-0.053289 |

-0.052921 |

0.000415 |

1.000000 |

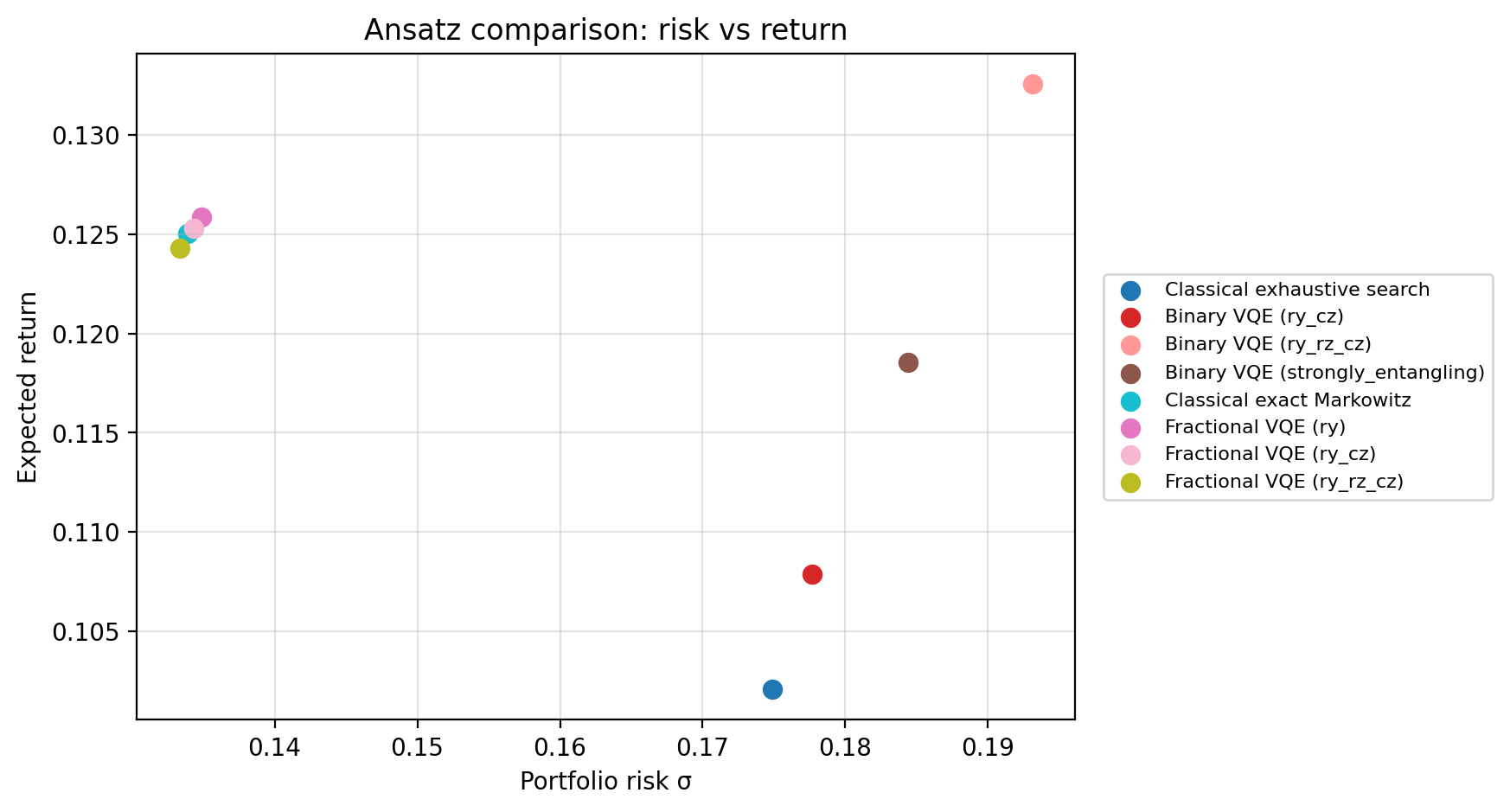

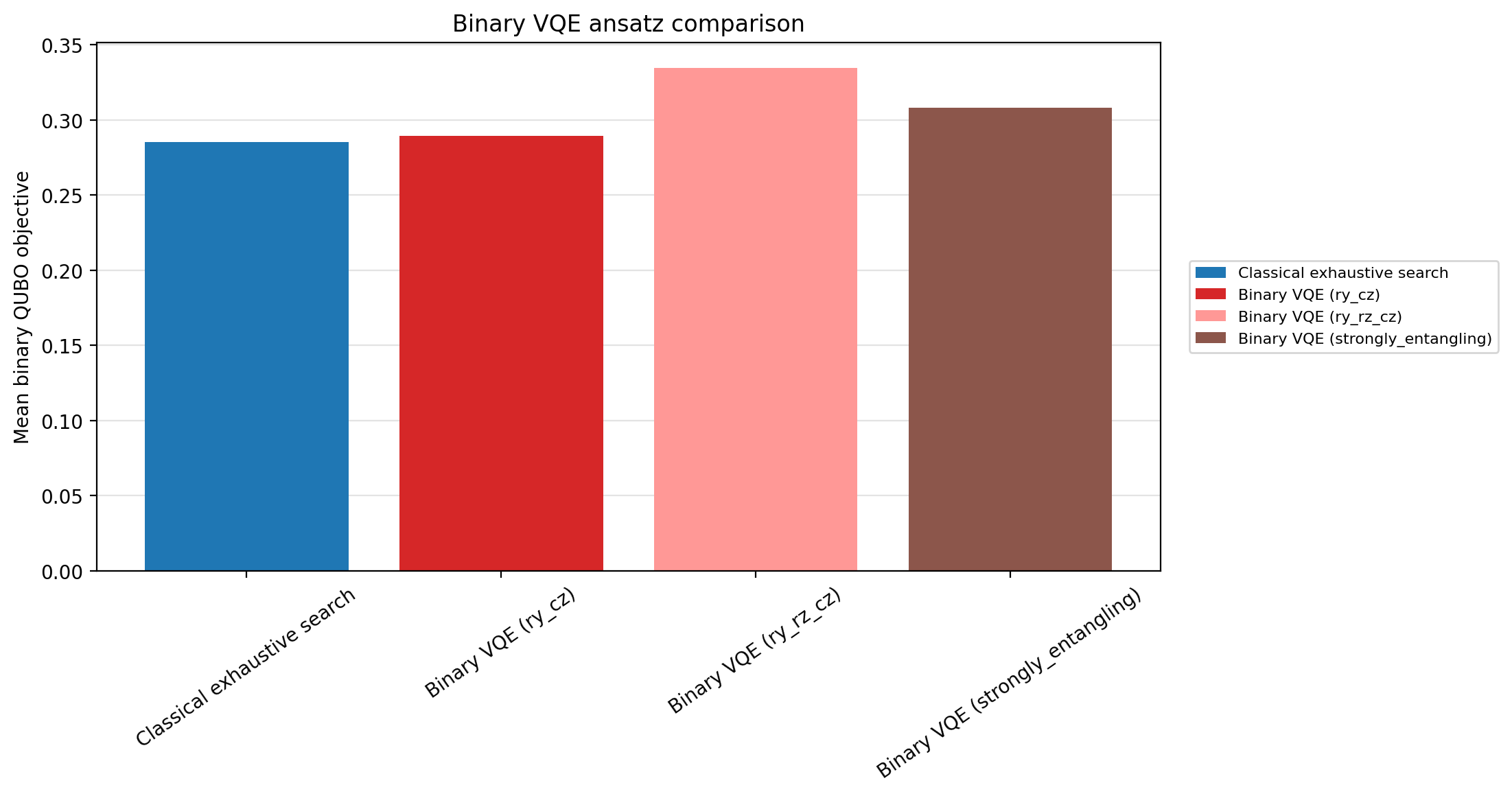

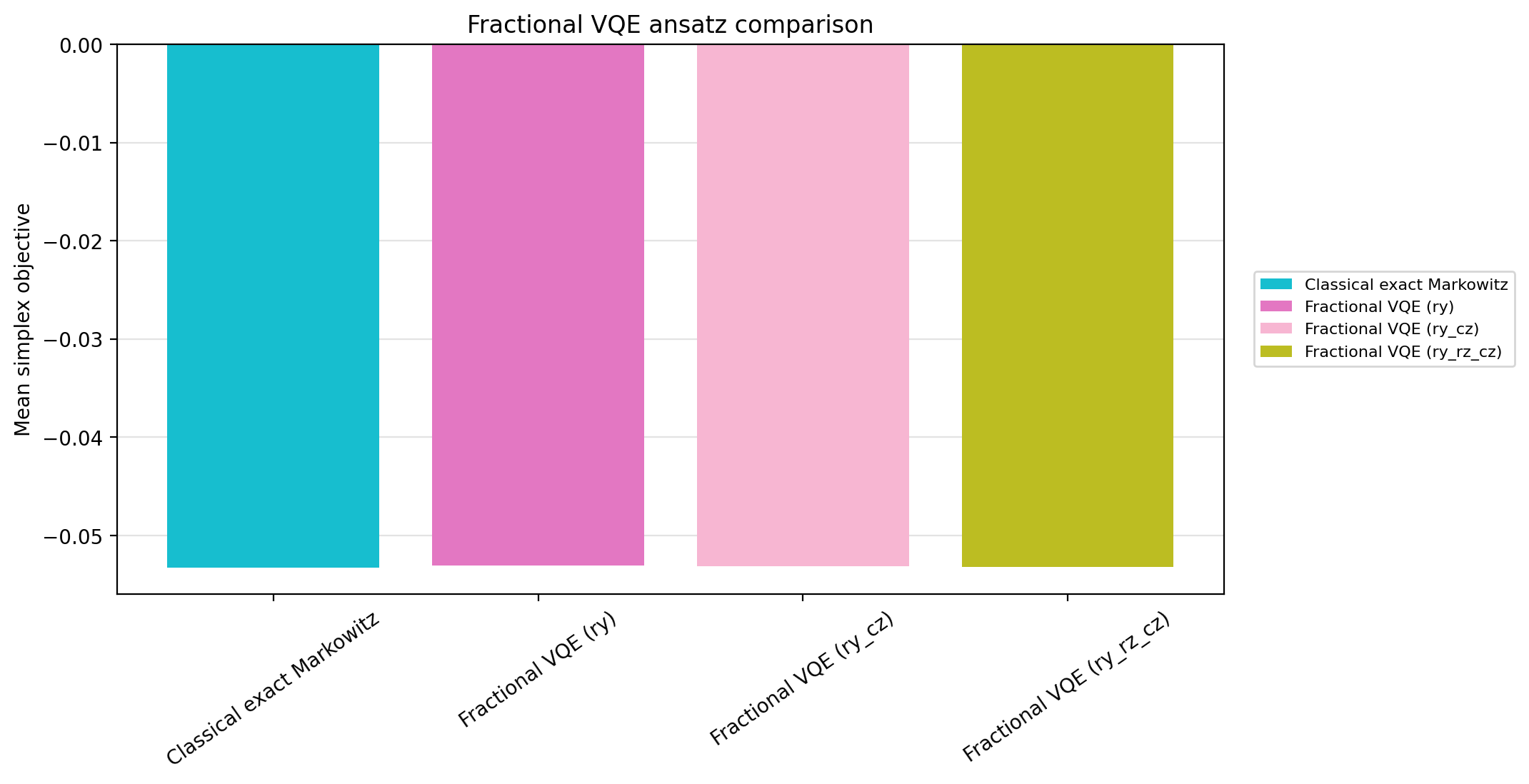

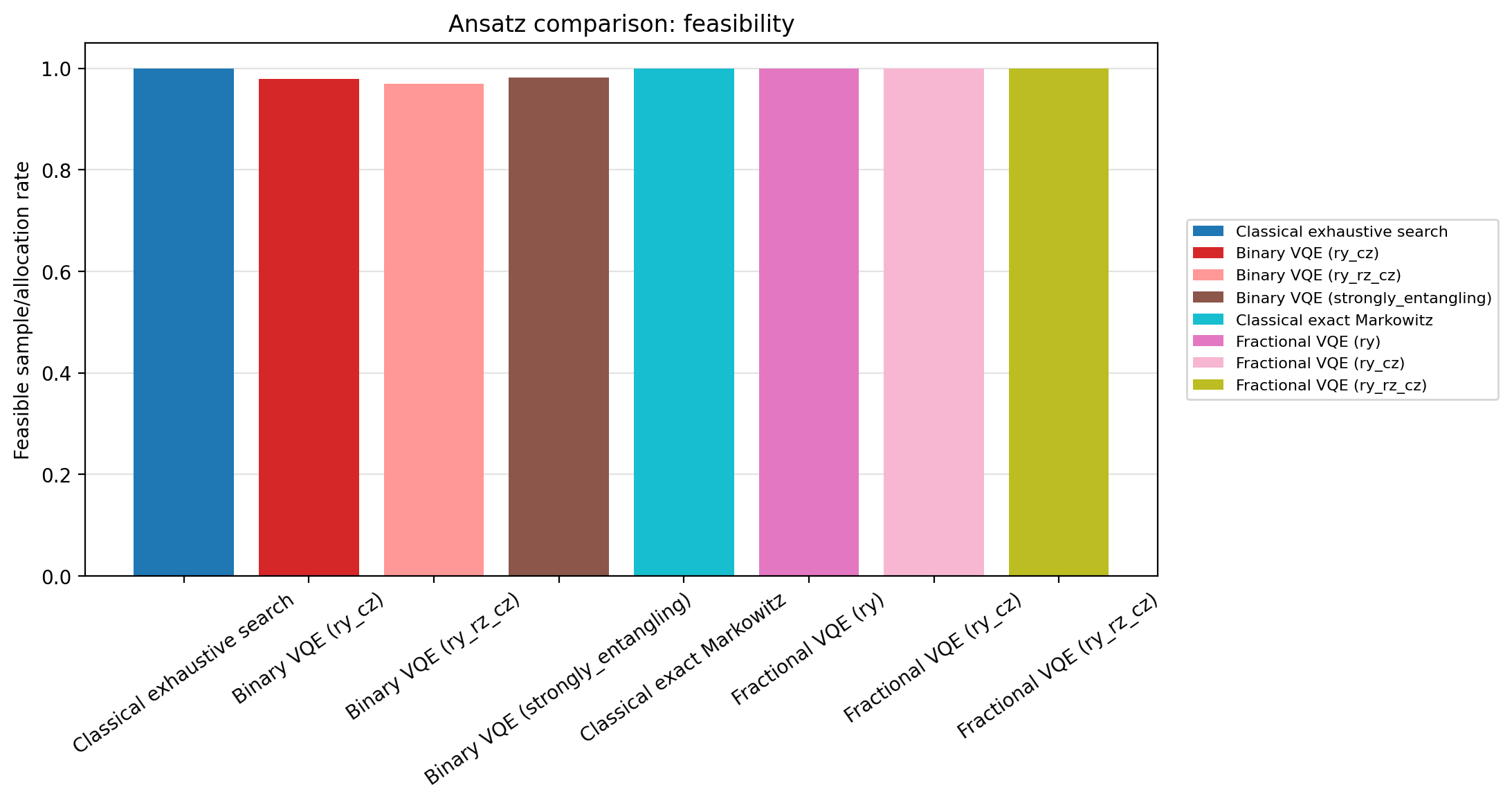

Ansatz Comparison Results¶

The ansatz comparison notebook is a compact pure-package client for the Binary VQE and Fractional VQE ansatz options. It writes results/ansatz_comparison.csv and keeps method/ansatz colors consistent across its risk-return, objective, and feasibility plots.

Regenerate it with:

python scripts/generate_ansatz_comparison.py

Synthetic Discrete Selection¶

Dataset |

Method |

Type |

λ |

K |

Selection |

Return |

Risk |

Variance |

Objective |

Feasible |

|---|---|---|---|---|---|---|---|---|---|---|

Synthetic binary toy |

Classical exhaustive search |

Classical |

5.0 |

2 |

|

0.300000 |

0.158114 |

0.025000 |

-0.175000 |

yes |

Synthetic binary toy |

Binary VQE Top-K |

Quantum |

5.0 |

2 |

|

0.320000 |

0.256905 |

0.066000 |

0.010000 |

yes |

Synthetic QAOA toy |

Classical exhaustive search |

Classical |

4.0 |

2 |

|

0.250000 |

0.360555 |

0.130000 |

0.270000 |

yes |

Synthetic QAOA toy |

QAOA X/XY best feasible |

Quantum |

4.0 |

2 |

|

0.250000 |

0.360555 |

0.130000 |

0.270000 |

yes |

Synthetic QAOA toy |

QAOA X/XY Top-K |

Quantum |

4.0 |

2 |

|

0.220000 |

0.387298 |

0.150000 |

0.380000 |

yes |

Synthetic Continuous Allocation¶

Dataset |

Method |

Type |

λ |

Selection or weights |

Return |

Risk |

Objective |

Feasible |

|---|---|---|---|---|---|---|---|---|

Synthetic fractional toy |

Classical Markowitz |

Classical |

5.0 |

|

0.142785 |

0.059812 |

-0.124897 |

yes |

Synthetic fractional toy |

Fractional VQE |

Quantum |

5.0 |

continuous allocation |

0.142792 |

0.059825 |

not printed |

simplex-normalized |

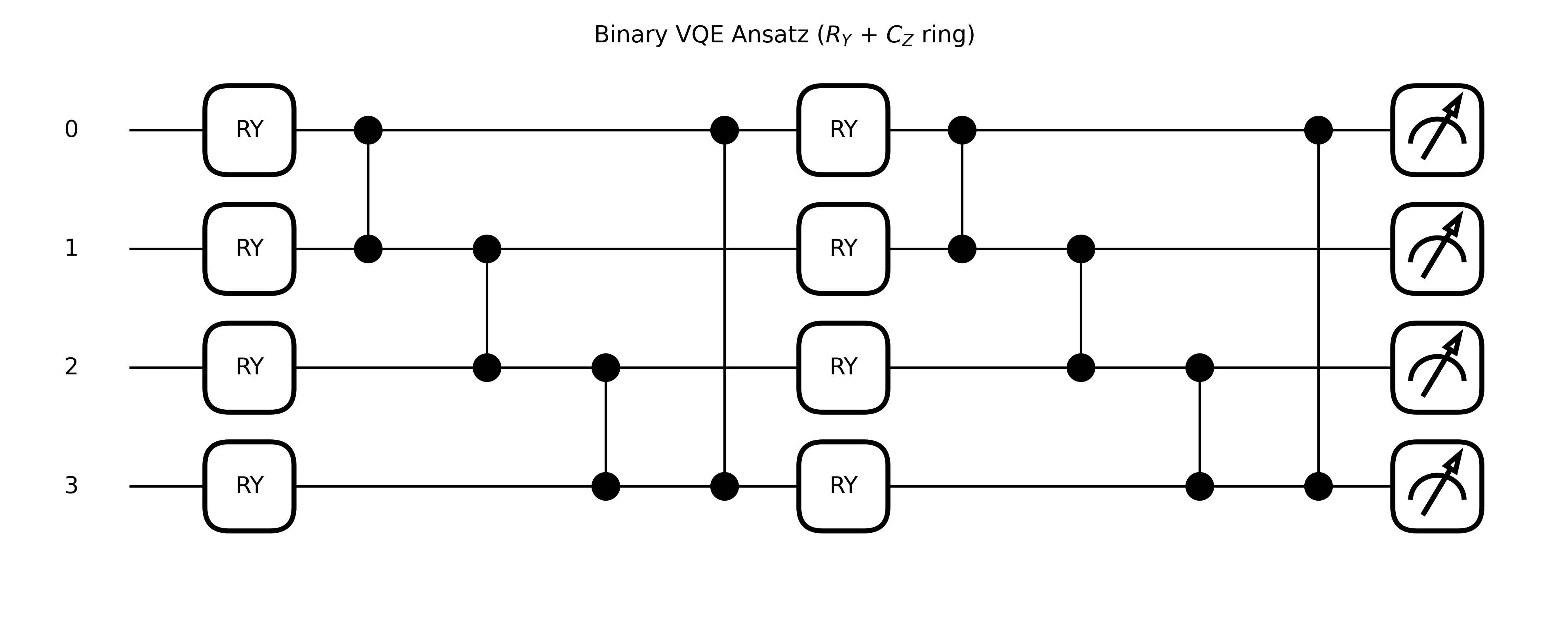

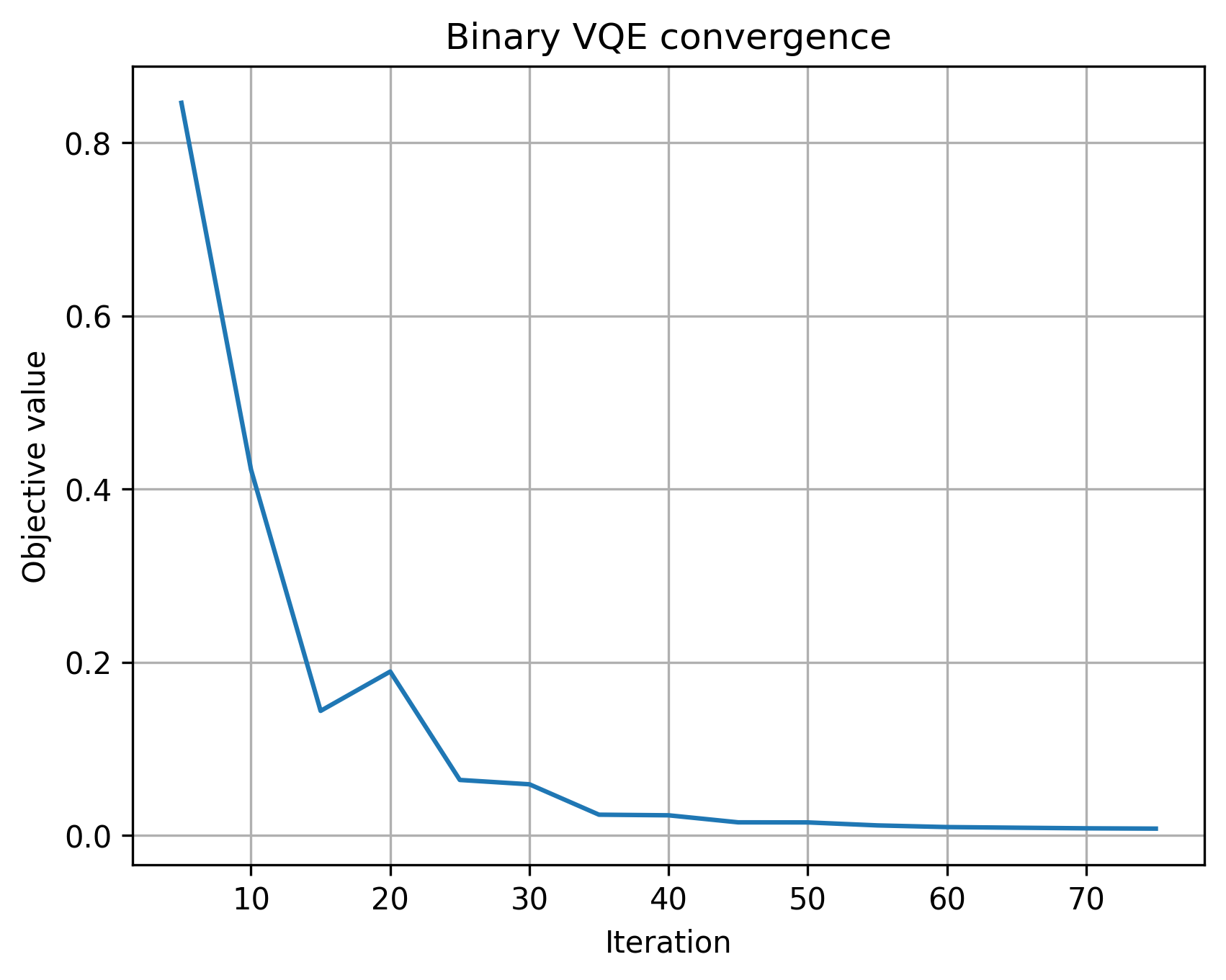

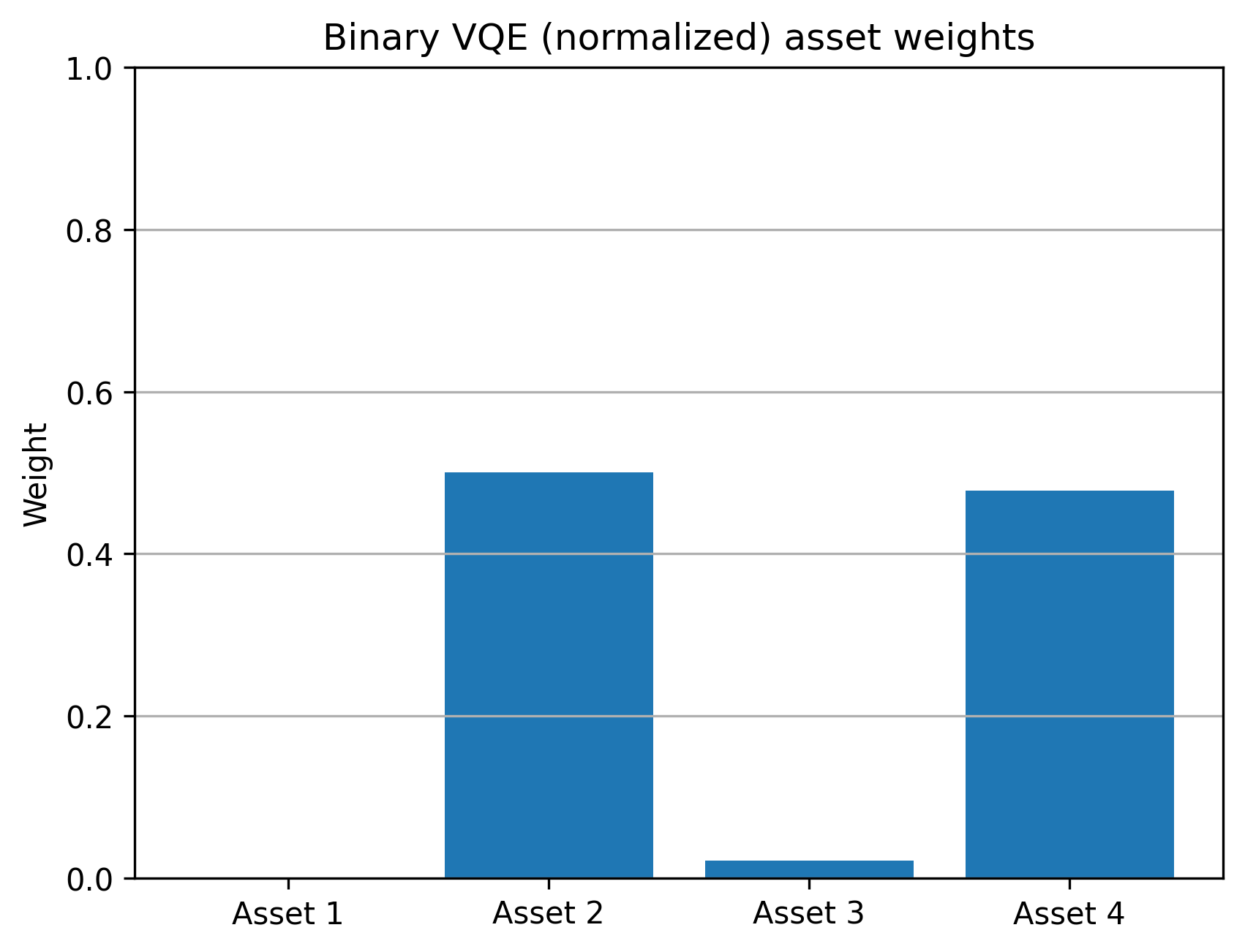

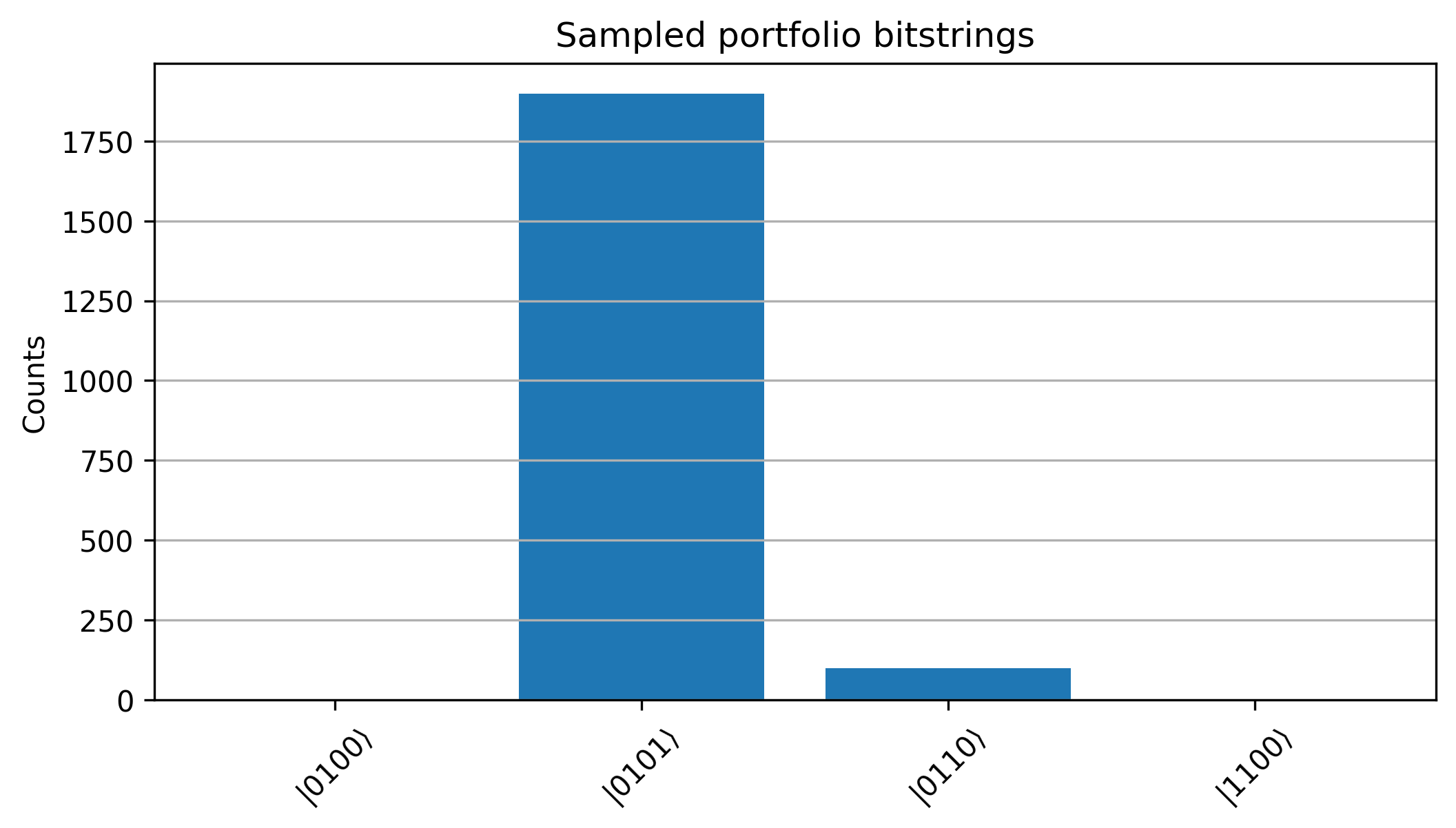

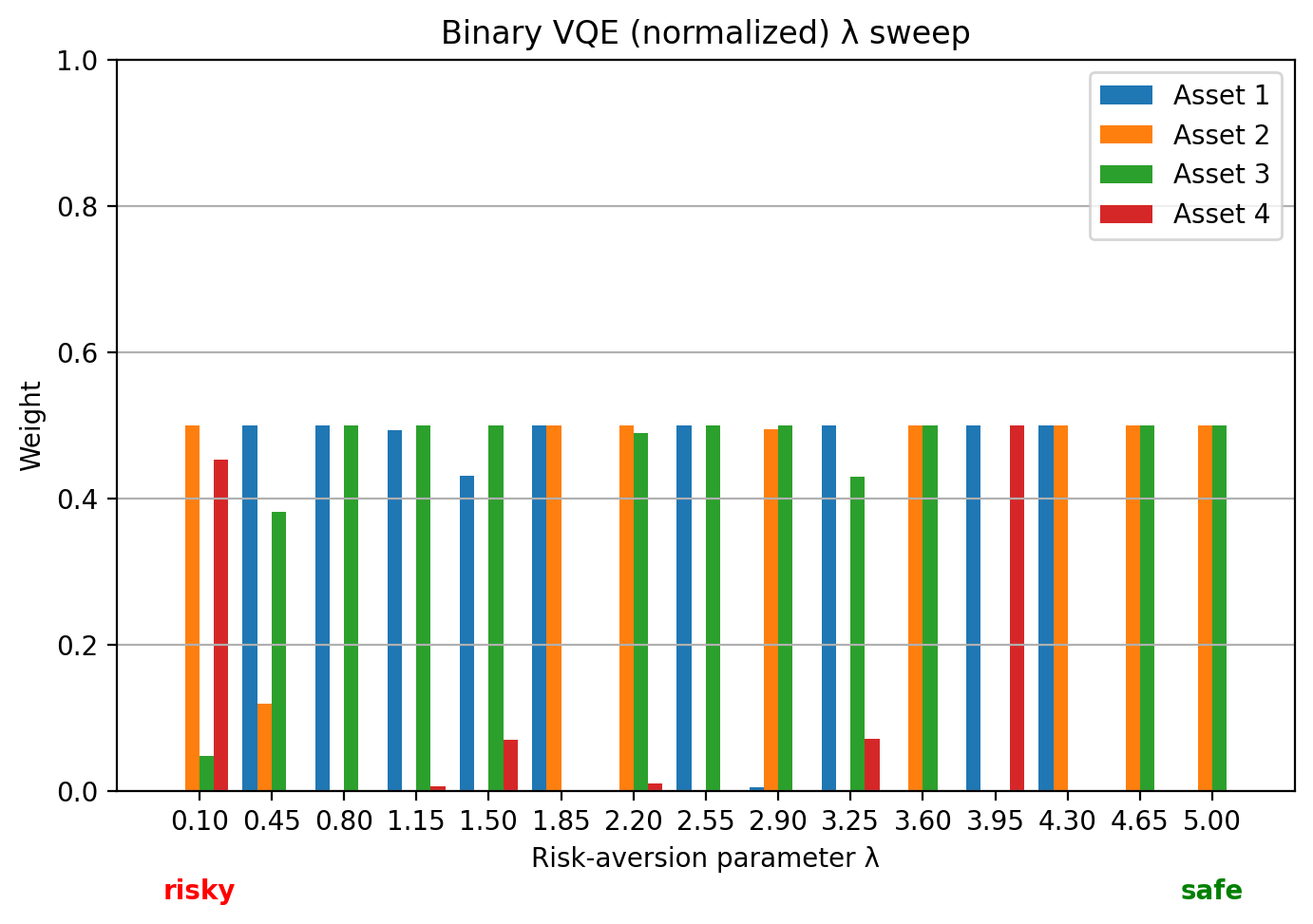

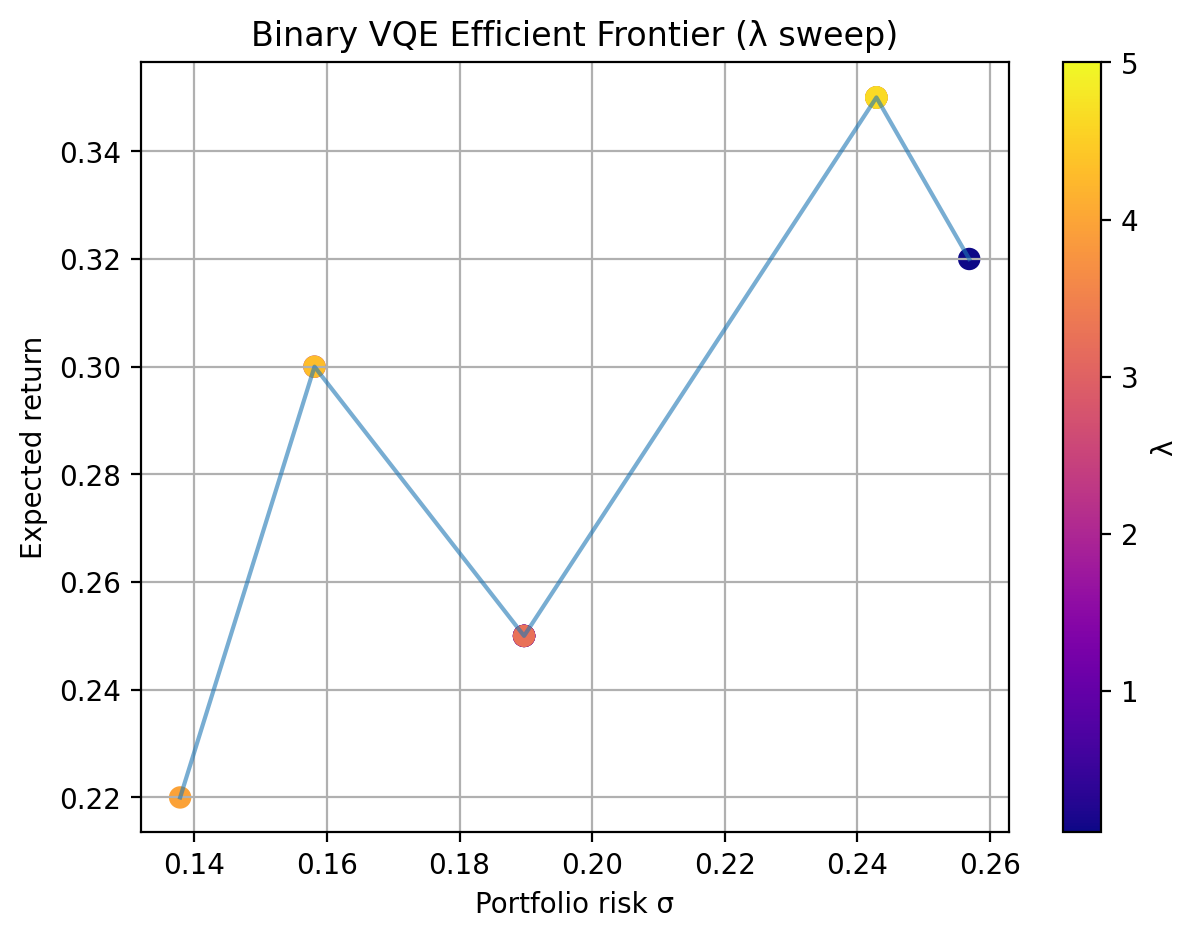

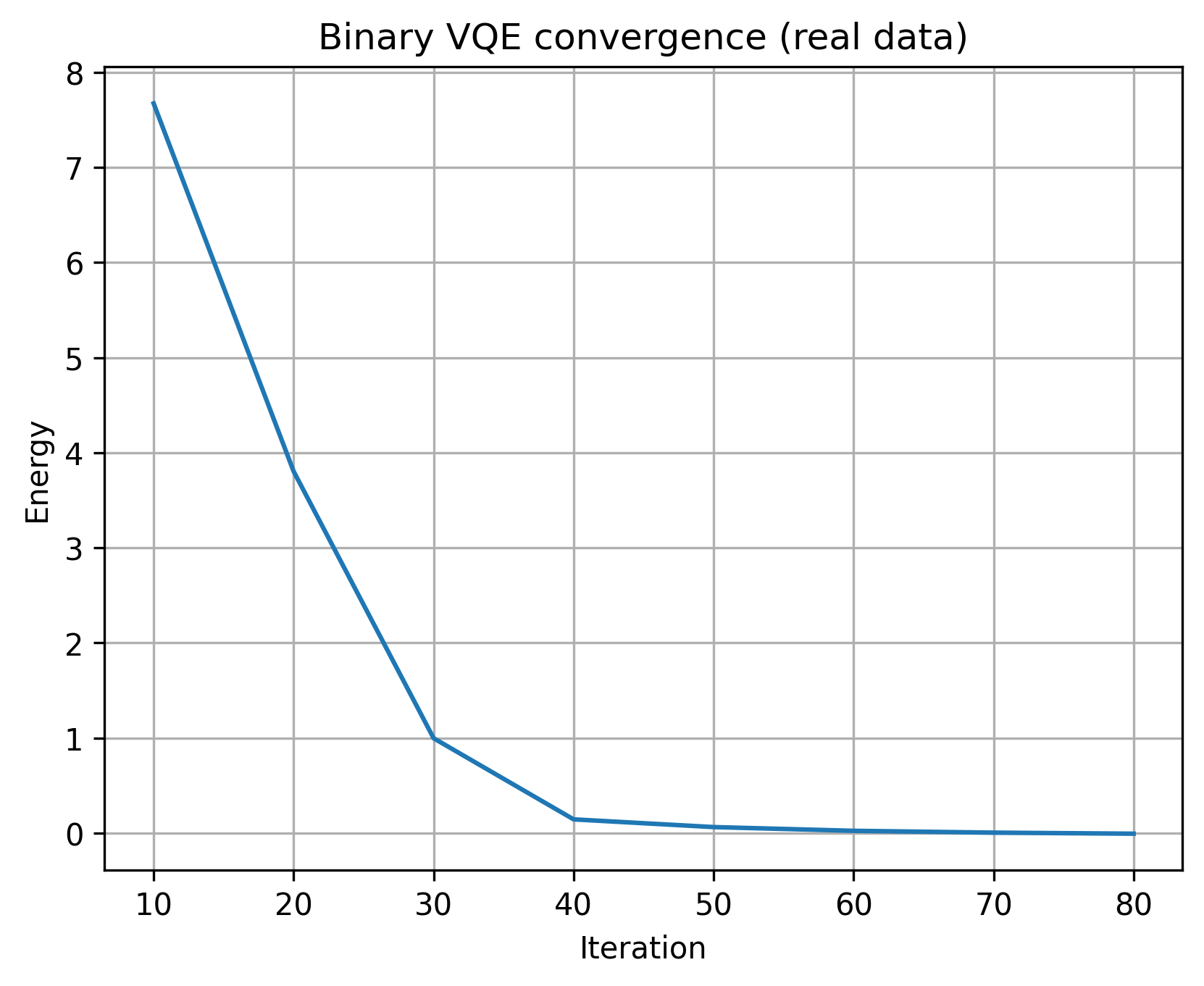

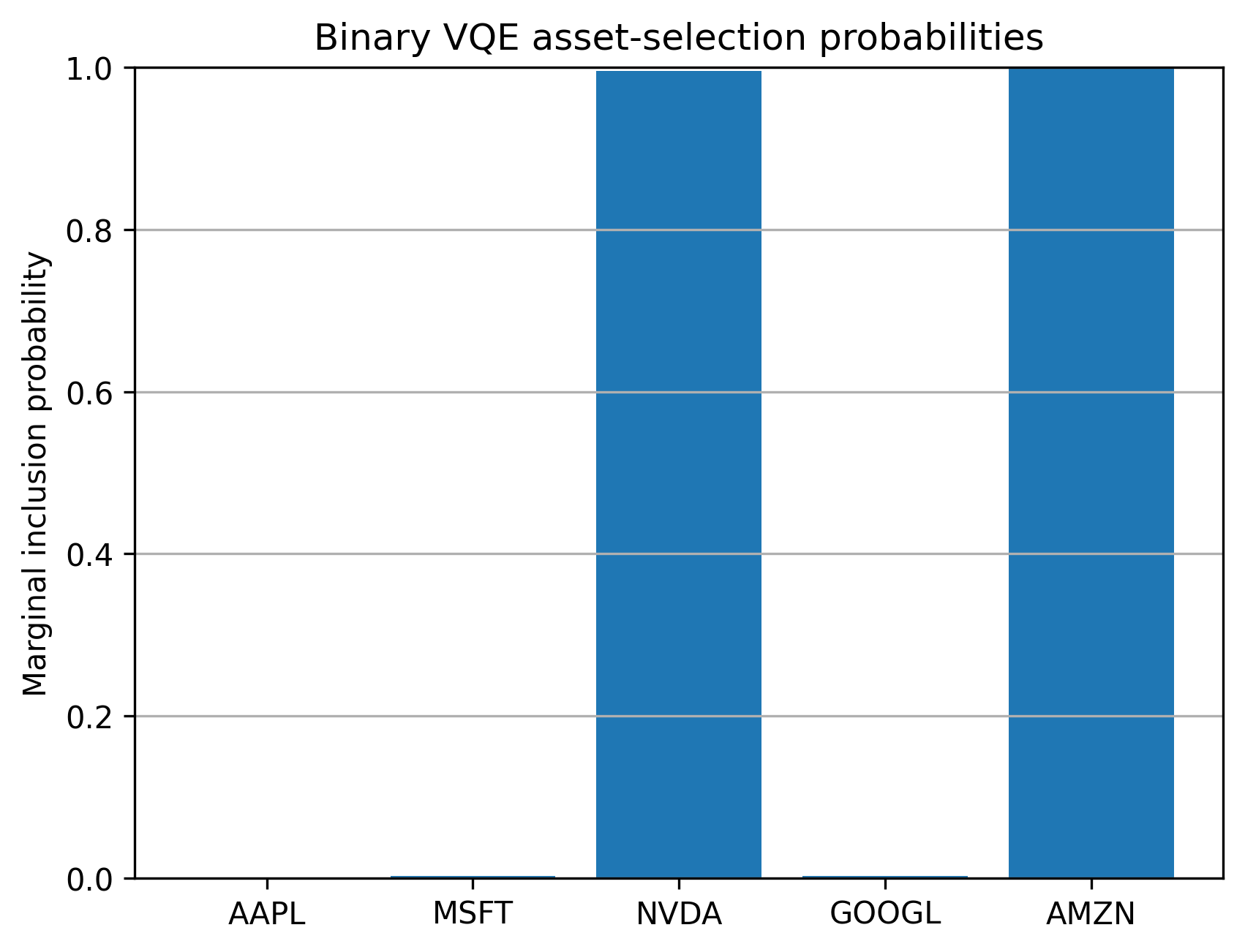

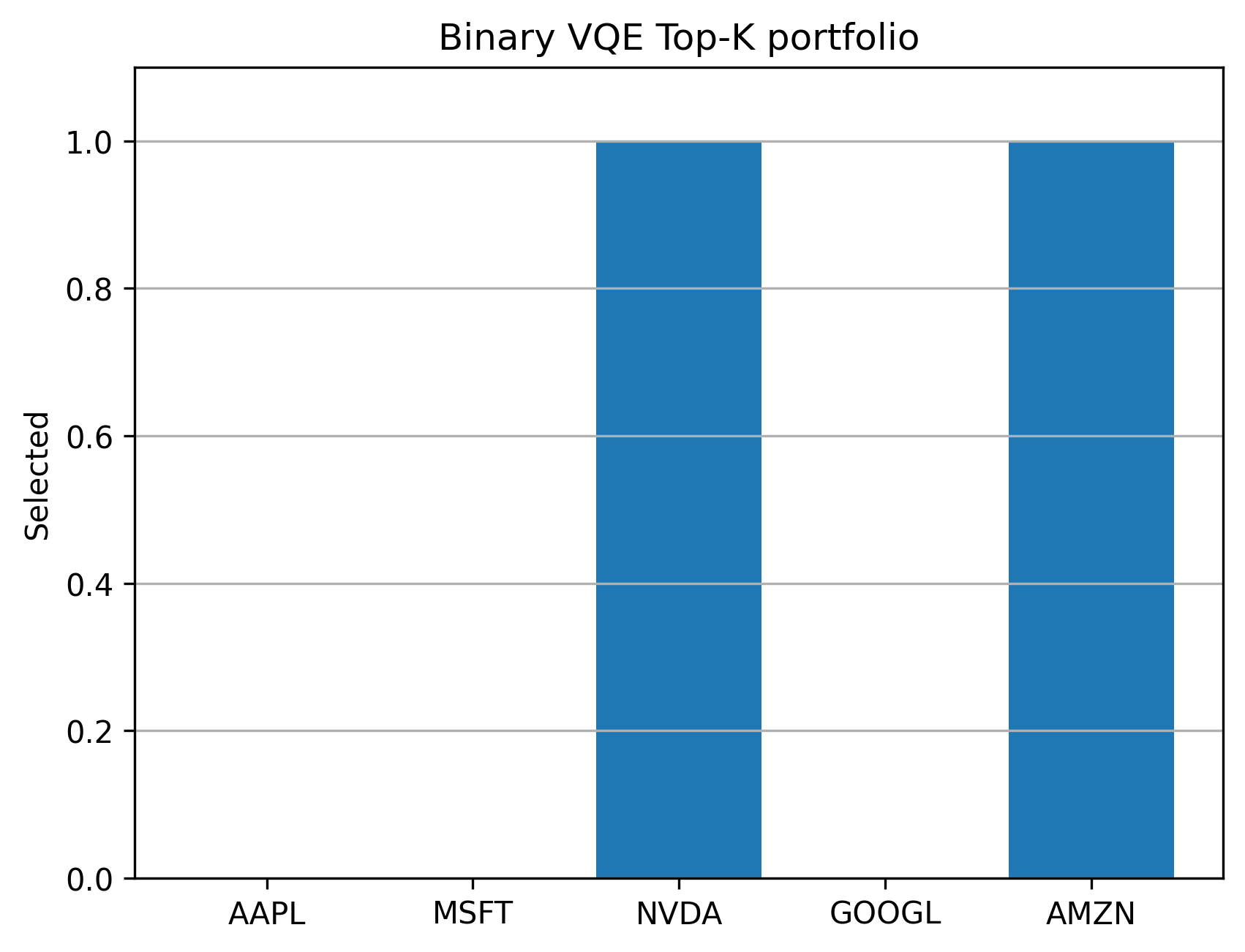

Binary VQE Synthetic Figures¶

Binary VQE solves a cardinality-constrained portfolio selection problem by mapping the QUBO objective to an Ising Hamiltonian and minimizing its expectation value with a parameterized circuit.

Artifact |

What it shows |

|---|---|

Circuit |

Hardware-efficient binary VQE ansatz used by the notebook client |

Convergence |

Optimizer cost trace over training steps |

Probabilities |

Selection probability distribution after optimization |

Bitstrings |

Most likely sampled portfolio bitstrings |

Lambda sweep |

Risk-return behavior as the risk-aversion parameter changes |

Efficient frontier |

Binary candidates compared across return/risk tradeoffs |

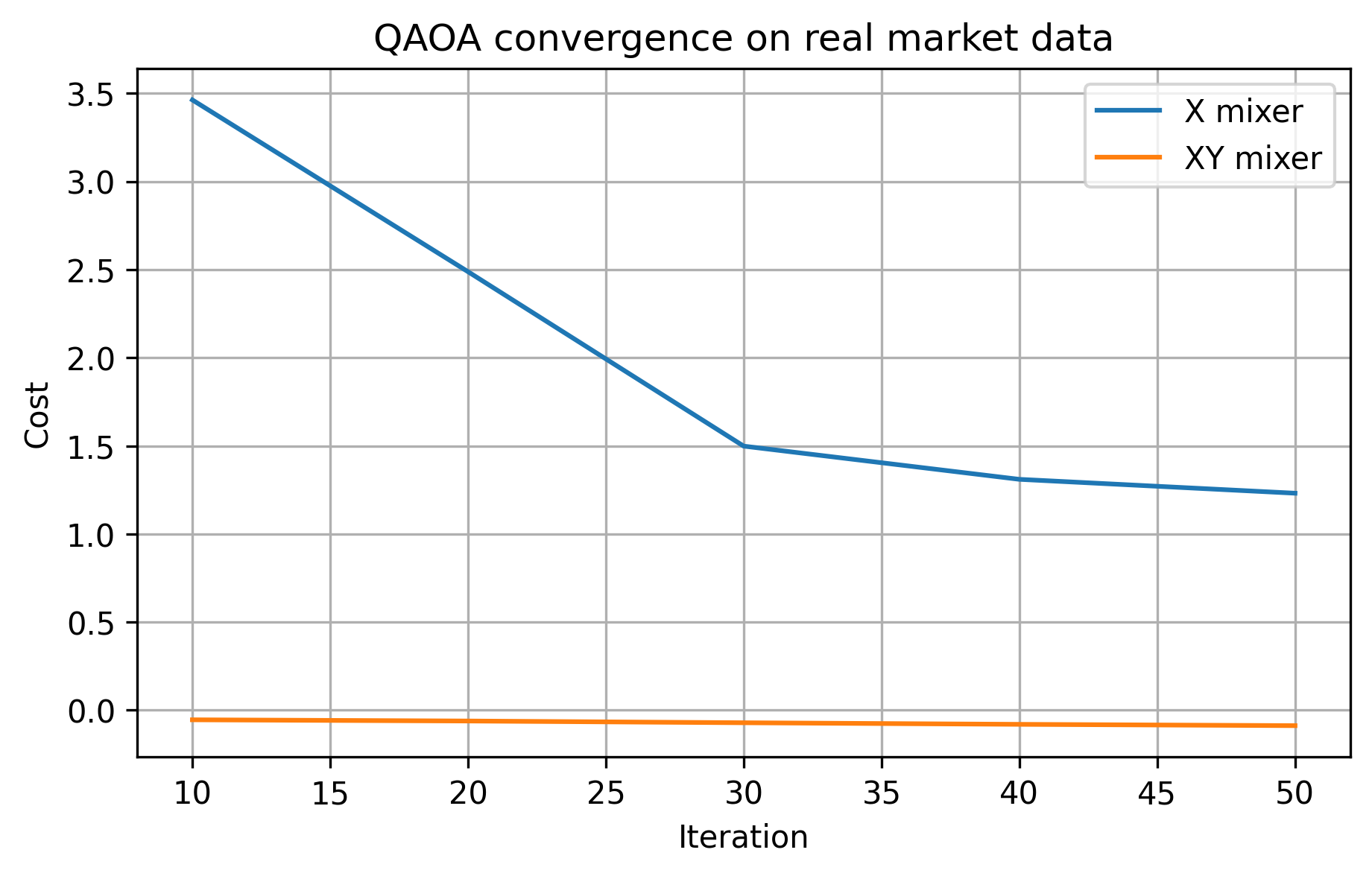

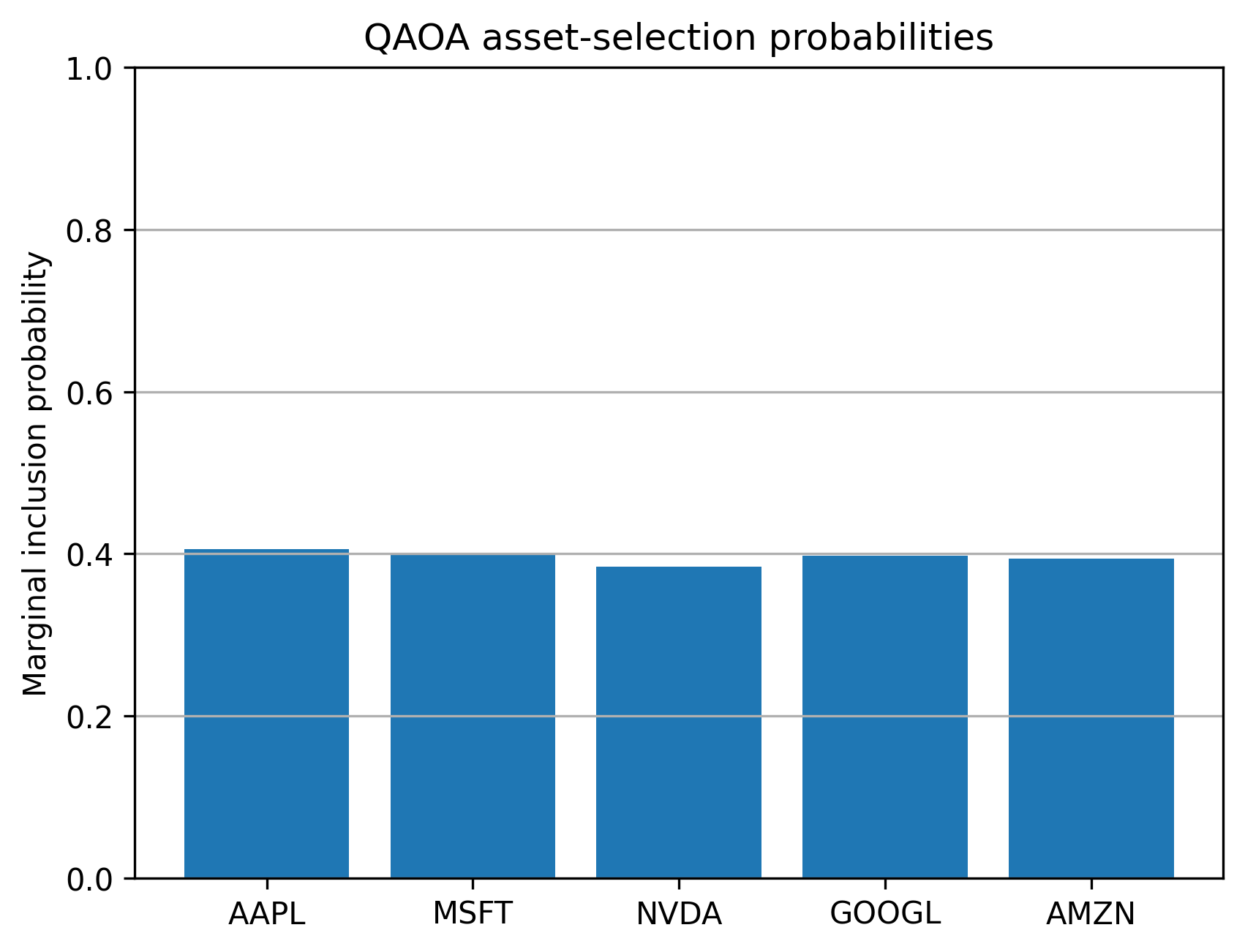

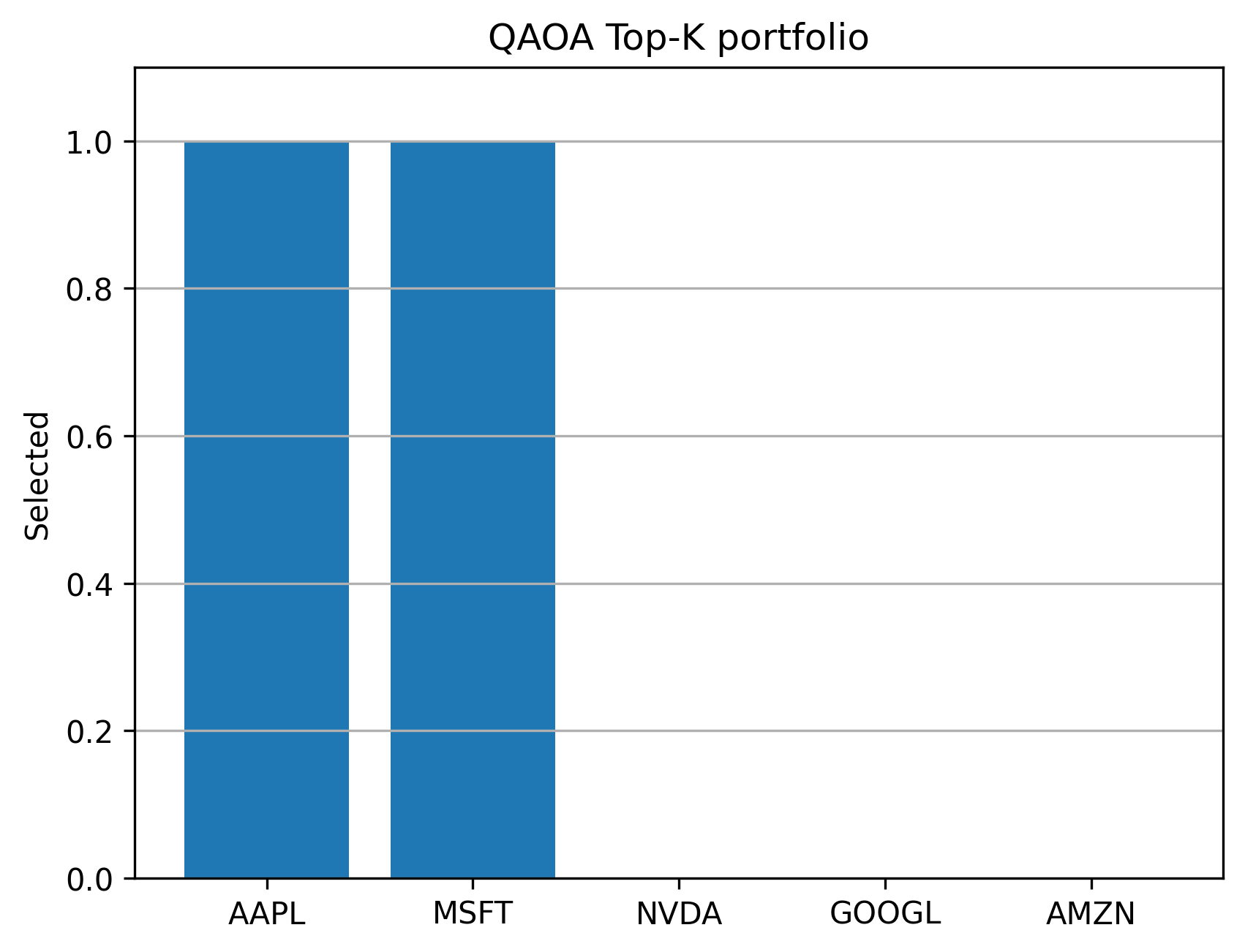

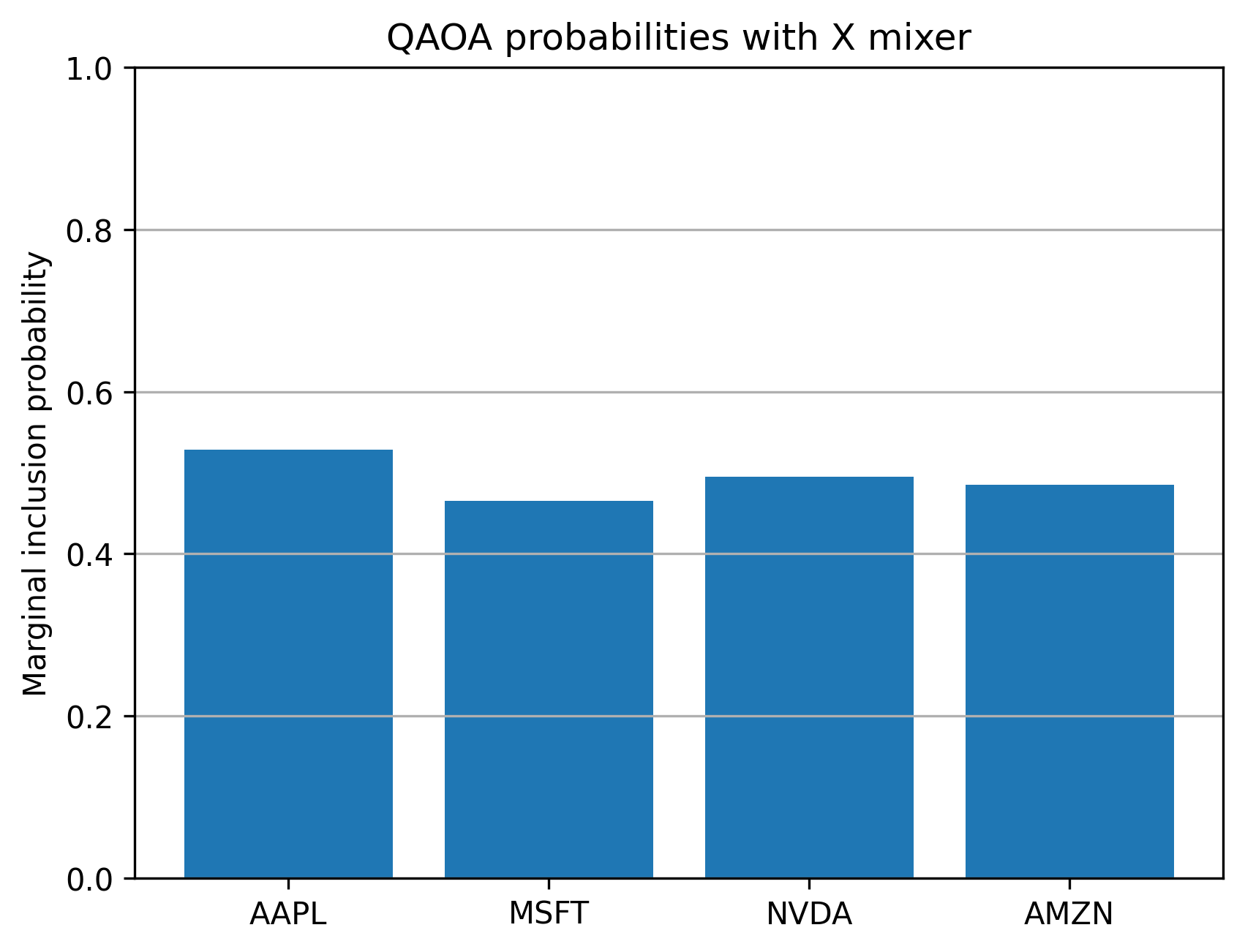

QAOA Synthetic Figures¶

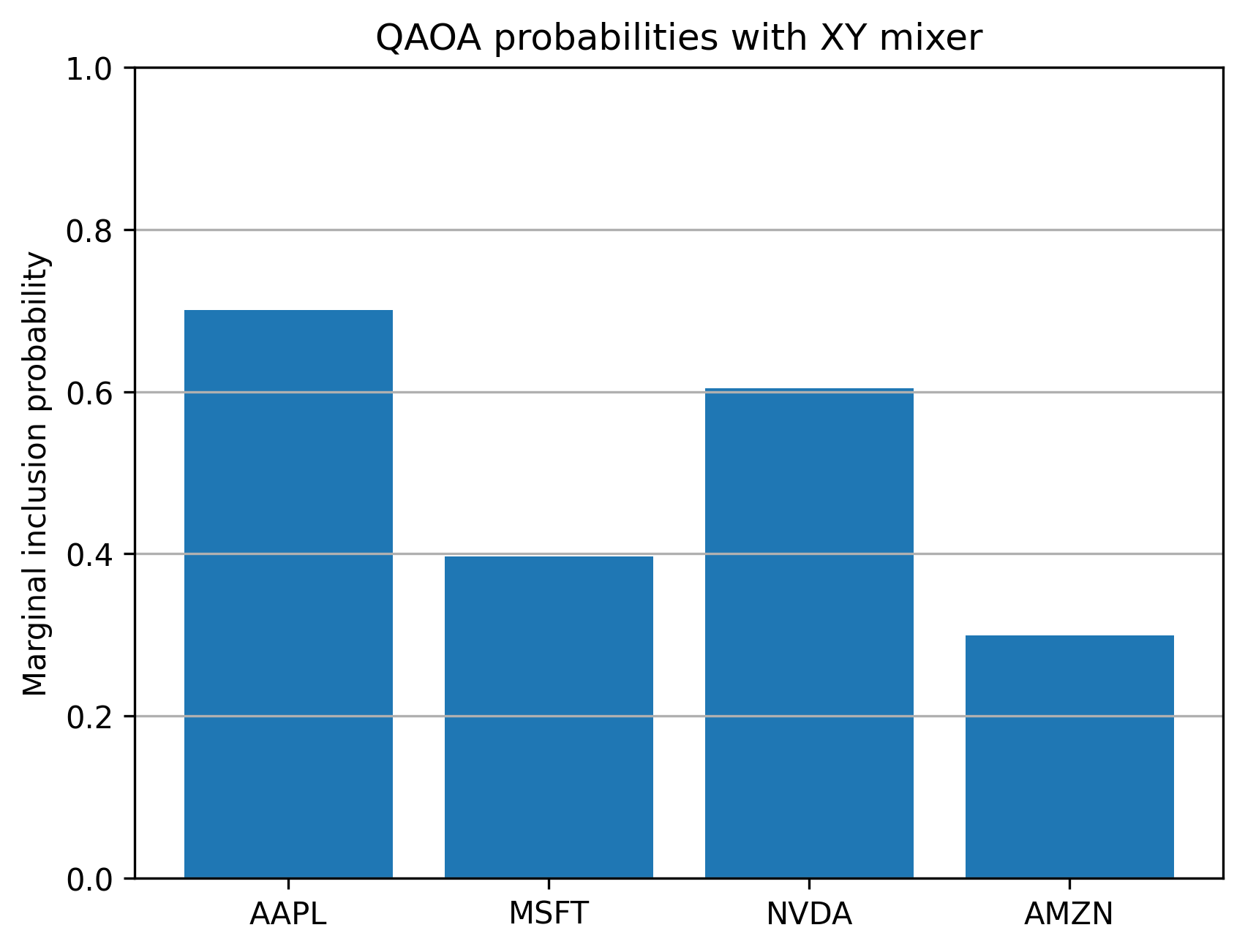

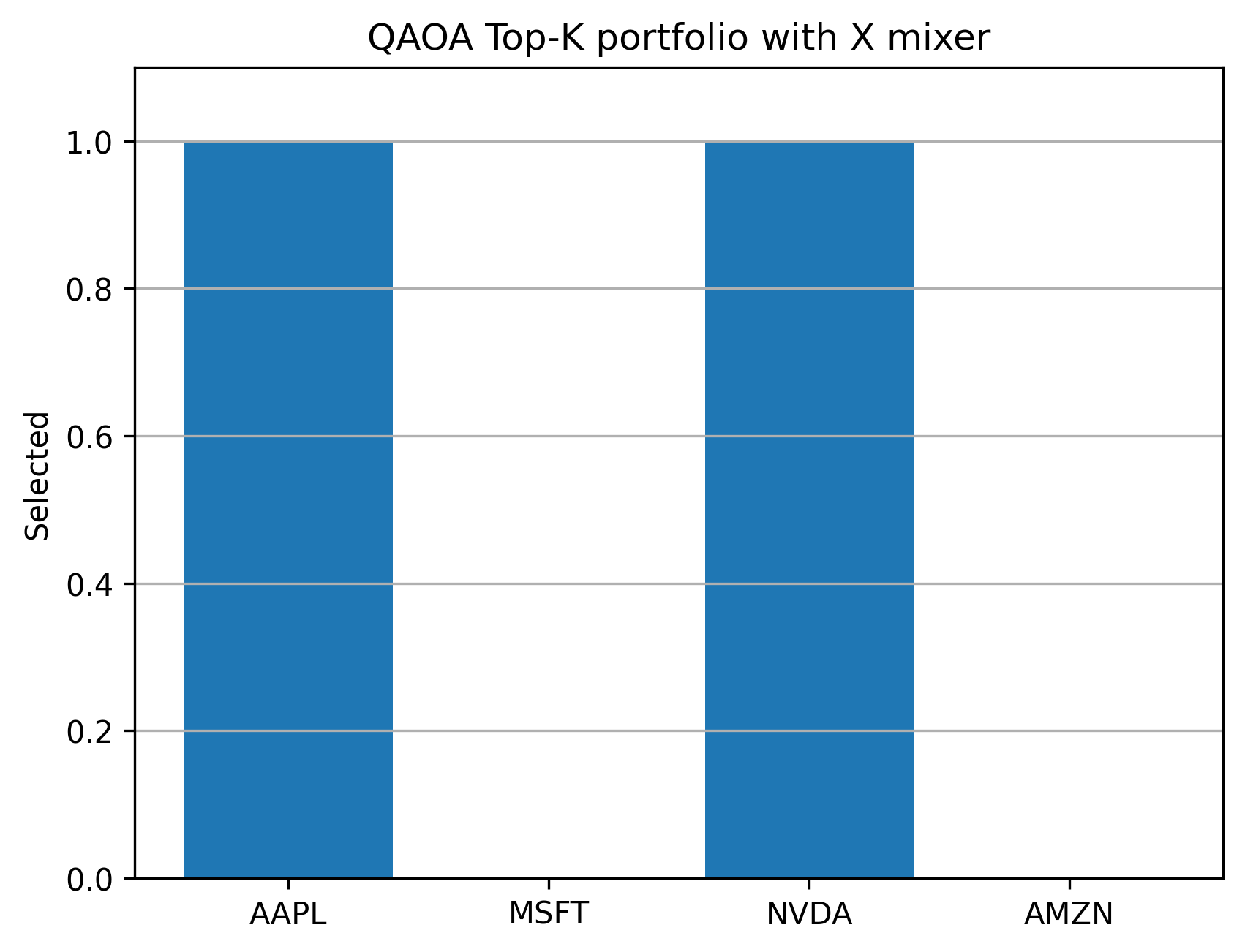

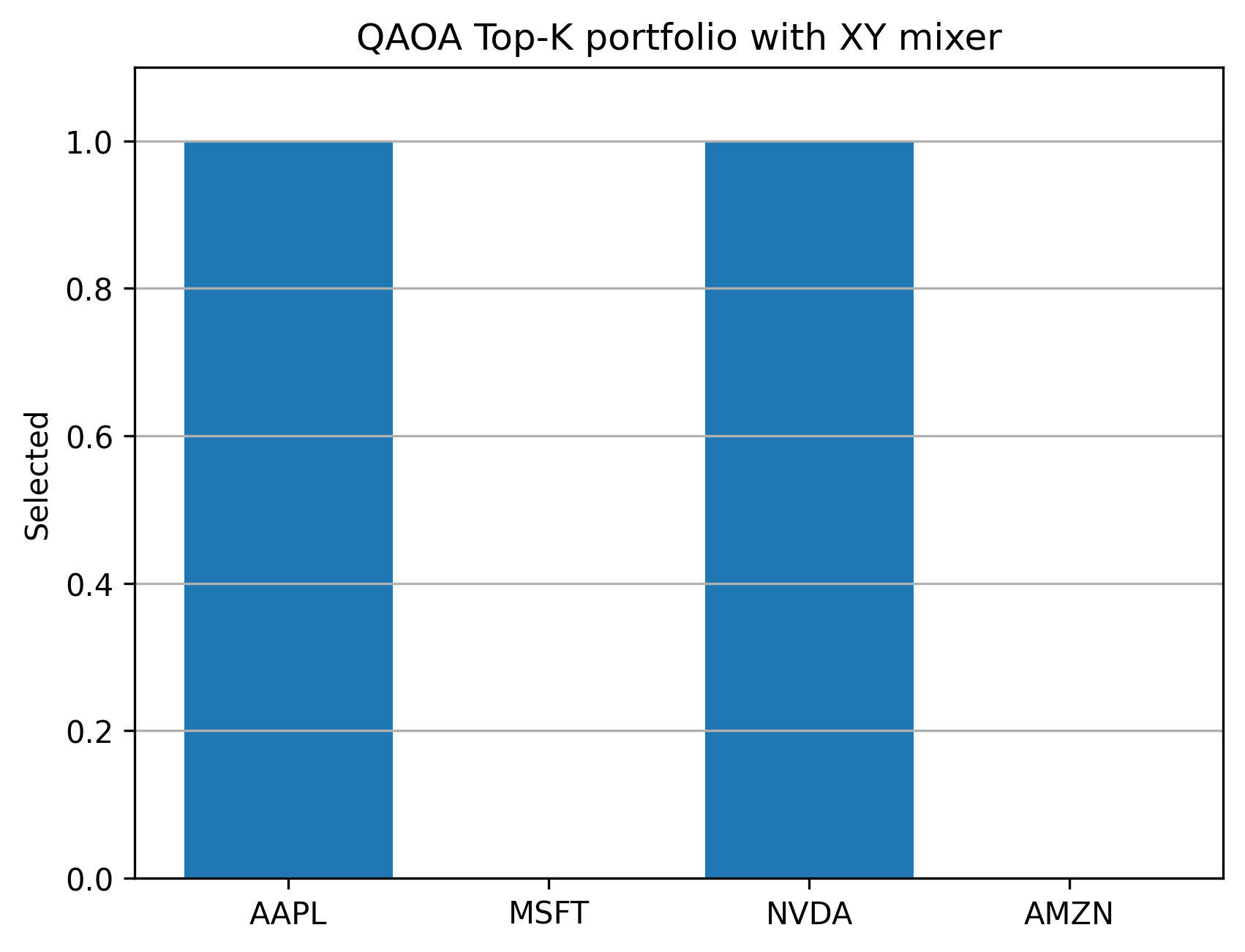

QAOA solves the binary portfolio objective with alternating cost and mixer unitaries. The synthetic notebook compares standard X-mixer sampling with constraint-aware XY-mixer behavior.

Artifact |

What it shows |

|---|---|

Candidate comparison |

Top-K, mode, and best-feasible sampled bitstrings |

Mixer comparison |

X and XY mixer behavior on the same binary objective |

Final portfolio metrics |

Return, quadratic risk, and objective for the selected feasible bitstring |

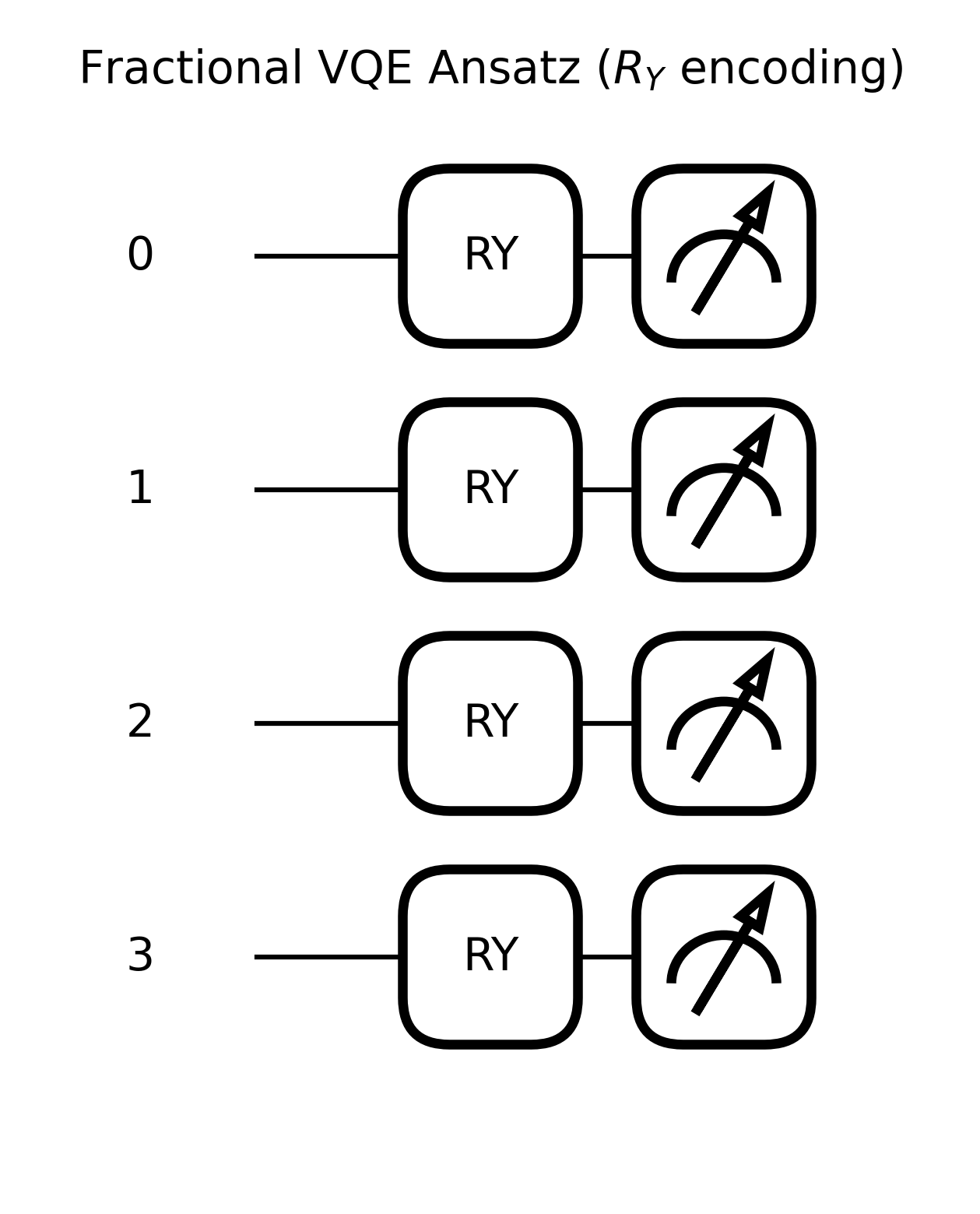

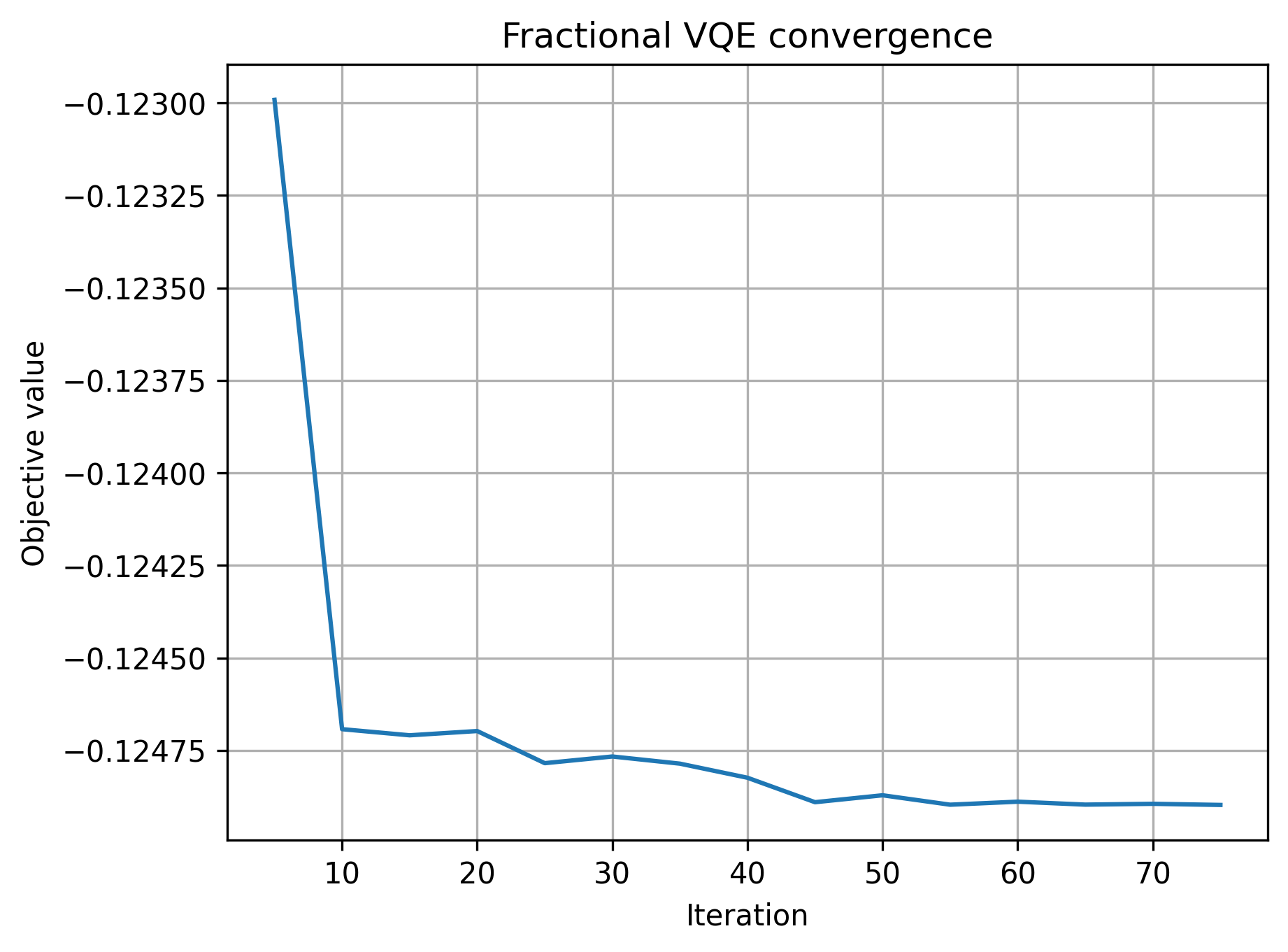

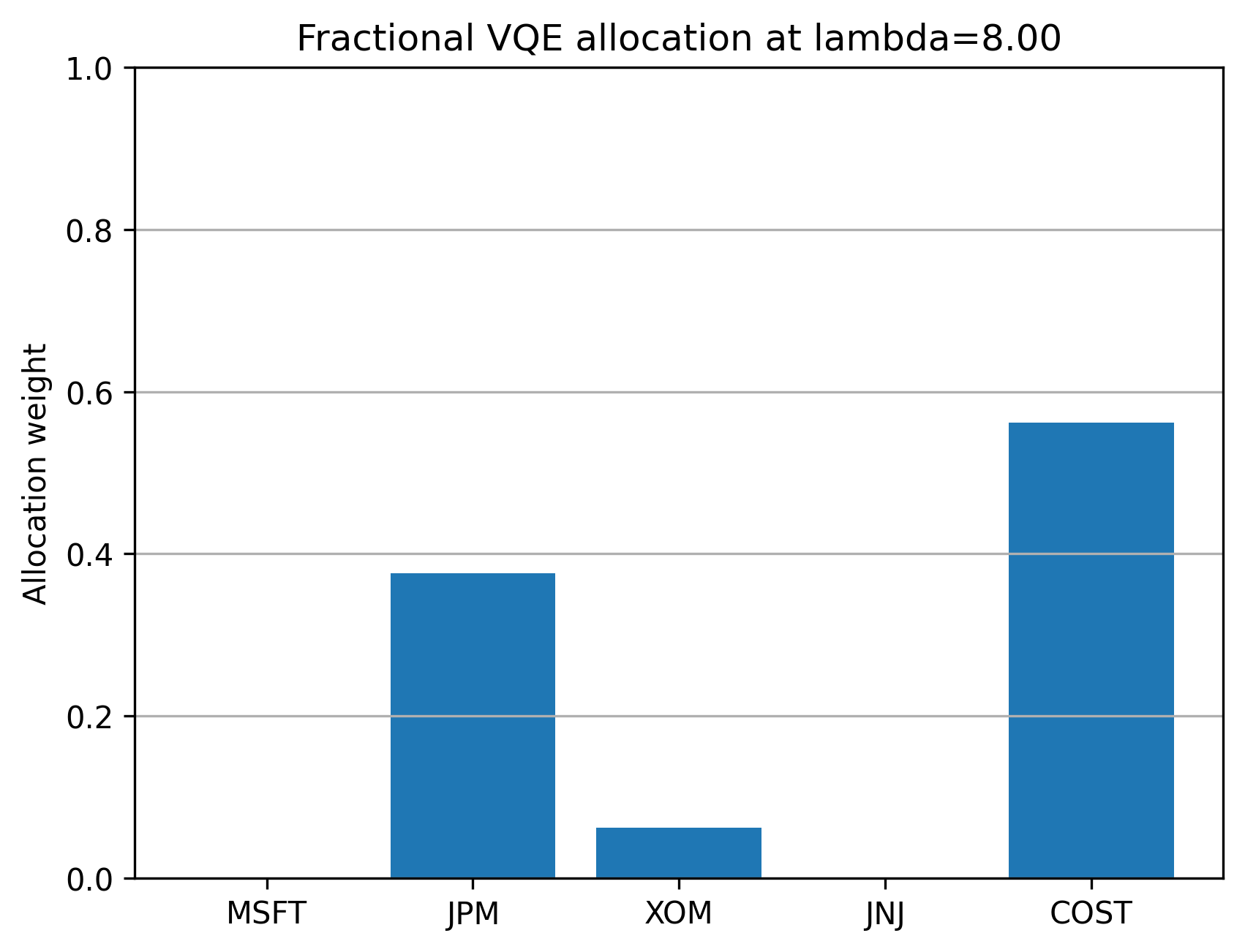

Fractional VQE Synthetic Figures¶

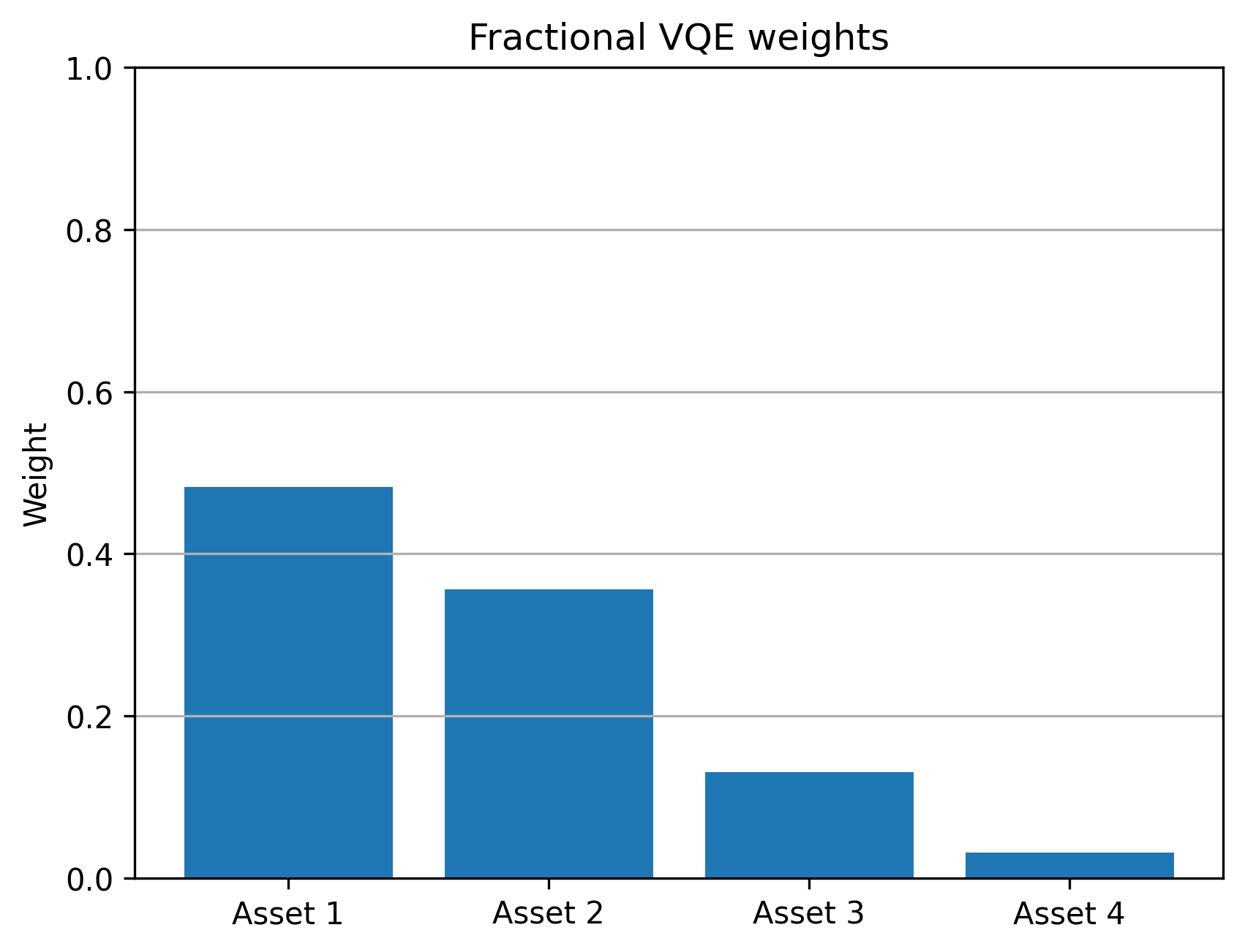

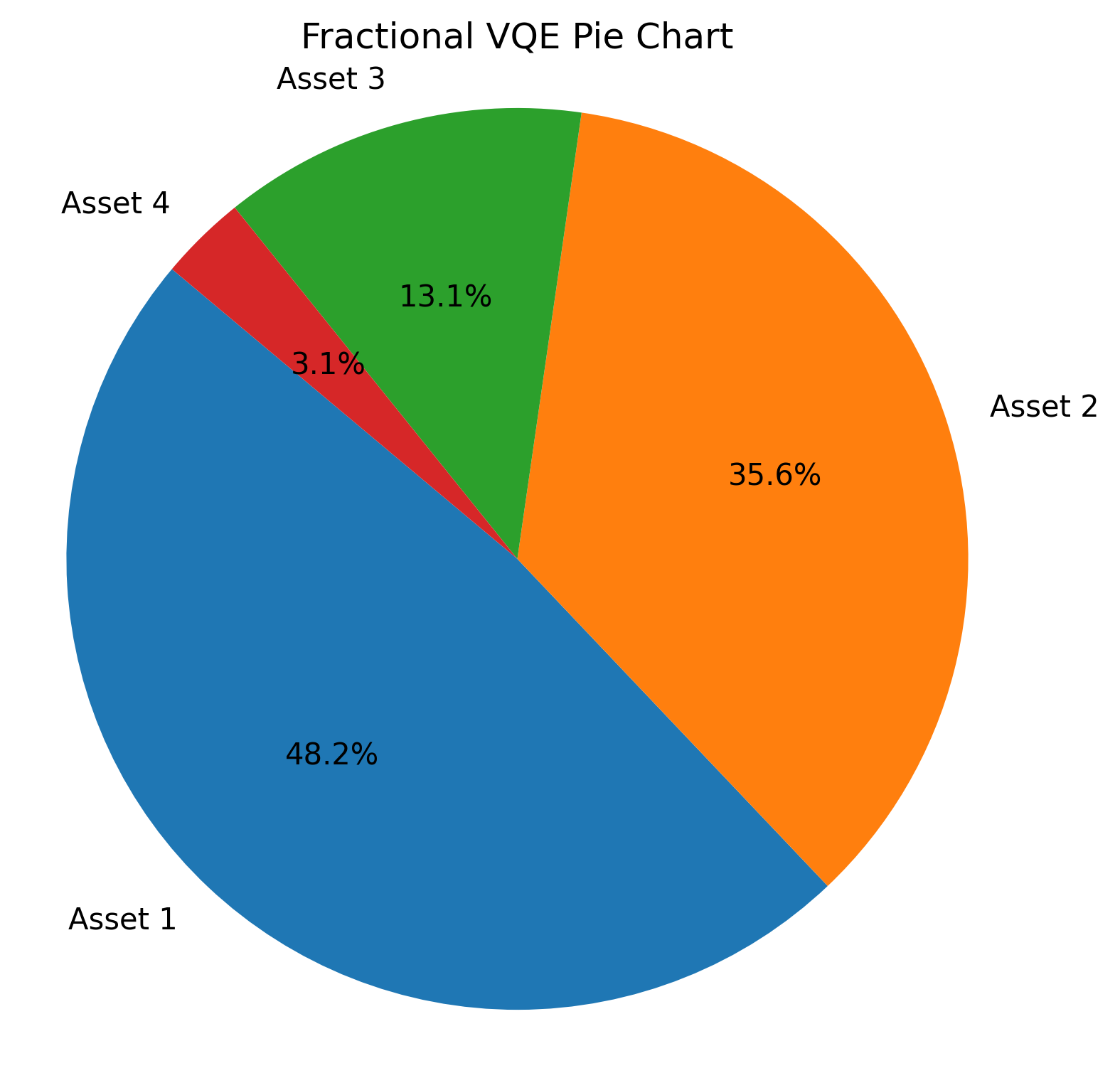

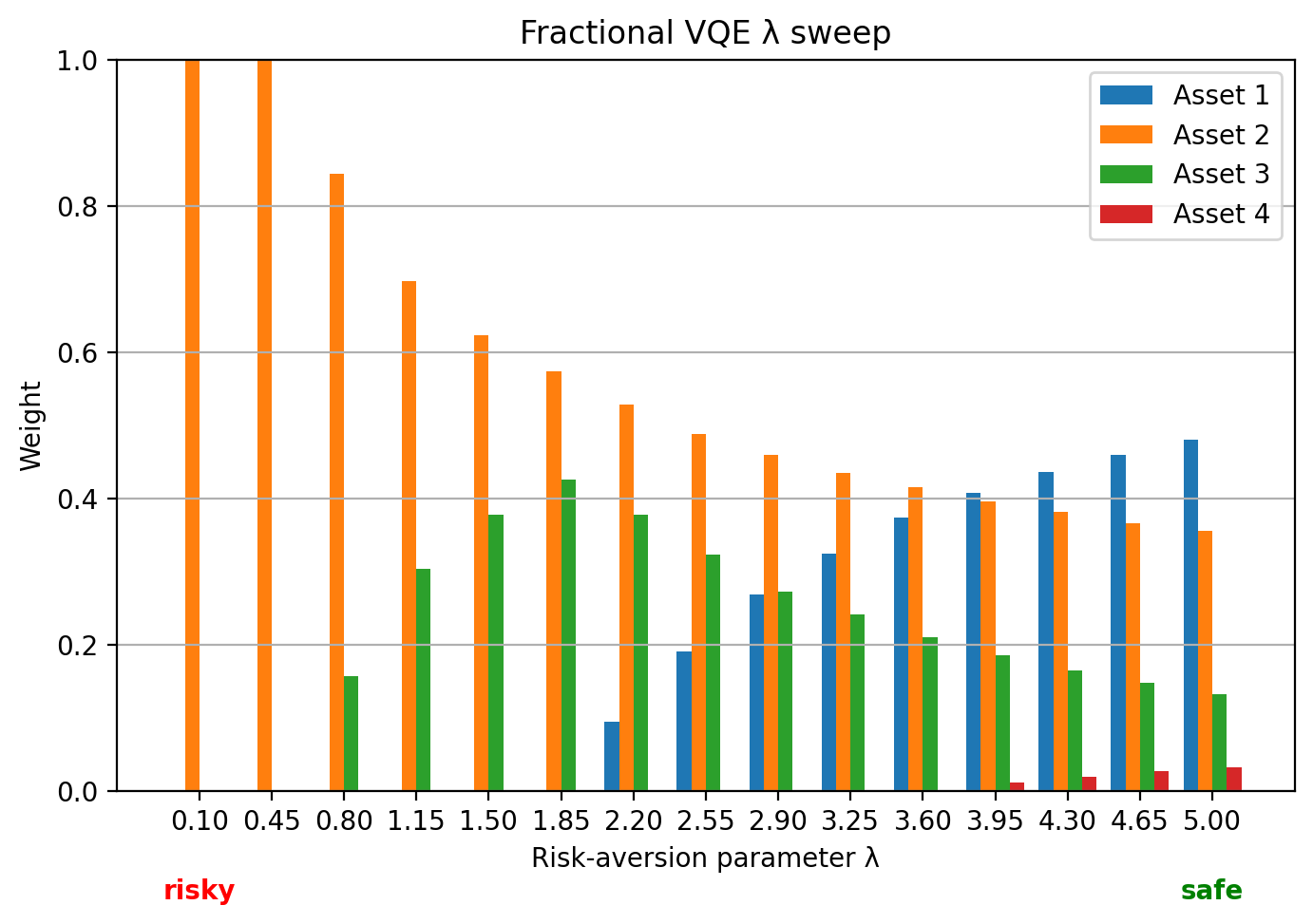

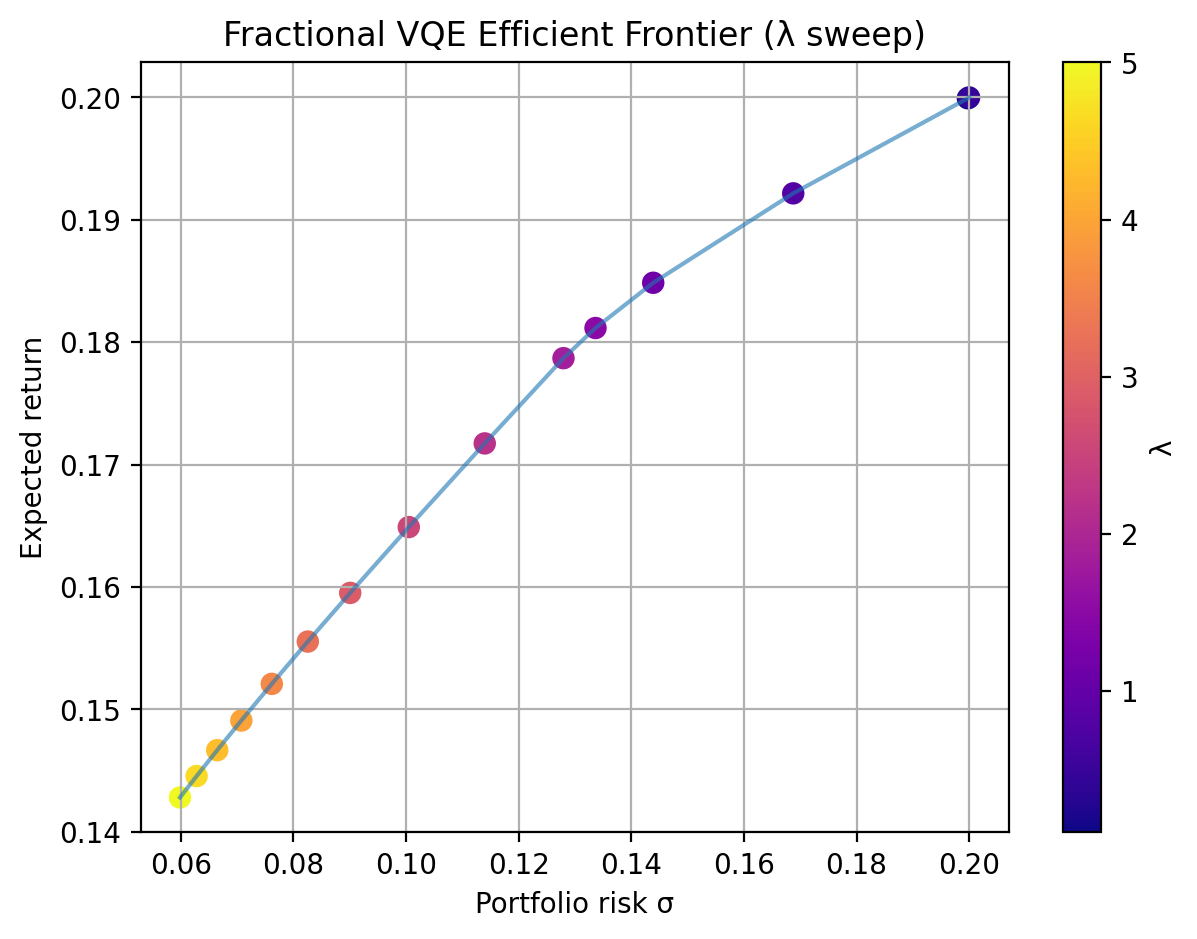

Fractional VQE optimizes long-only continuous allocations on the simplex. This complements binary selection by producing allocation weights directly rather than choosing a fixed-size subset.

Artifact |

What it shows |

|---|---|

Circuit |

Fractional VQE ansatz used for continuous allocation |

Convergence |

Optimizer behavior for the fractional objective |

Probabilities |

Allocation-related distribution from the fractional workflow |

Final allocation |

Portfolio weights displayed as a pie chart |

Lambda sweep |

Allocation changes over risk-aversion settings |

Efficient frontier |

Fractional allocation frontier from optimized portfolios |

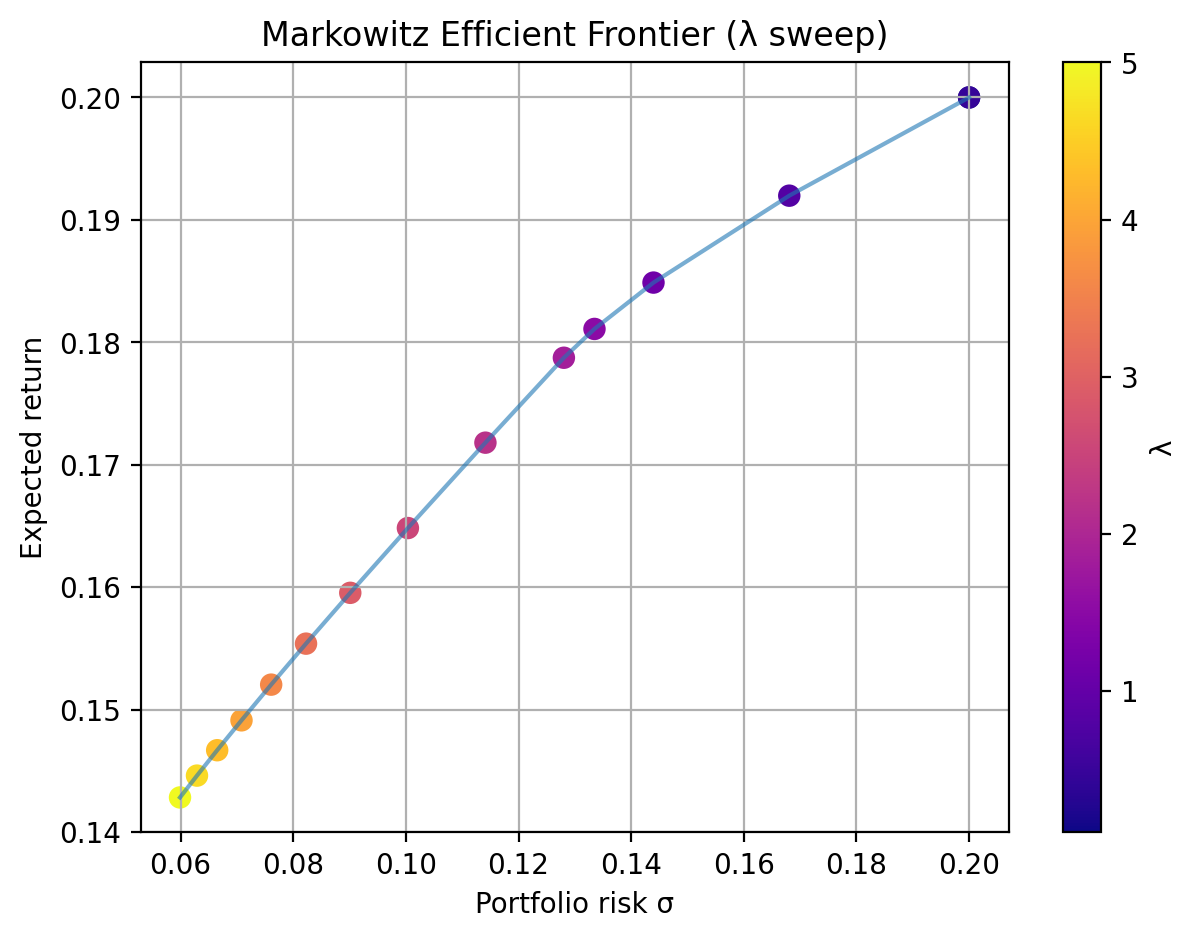

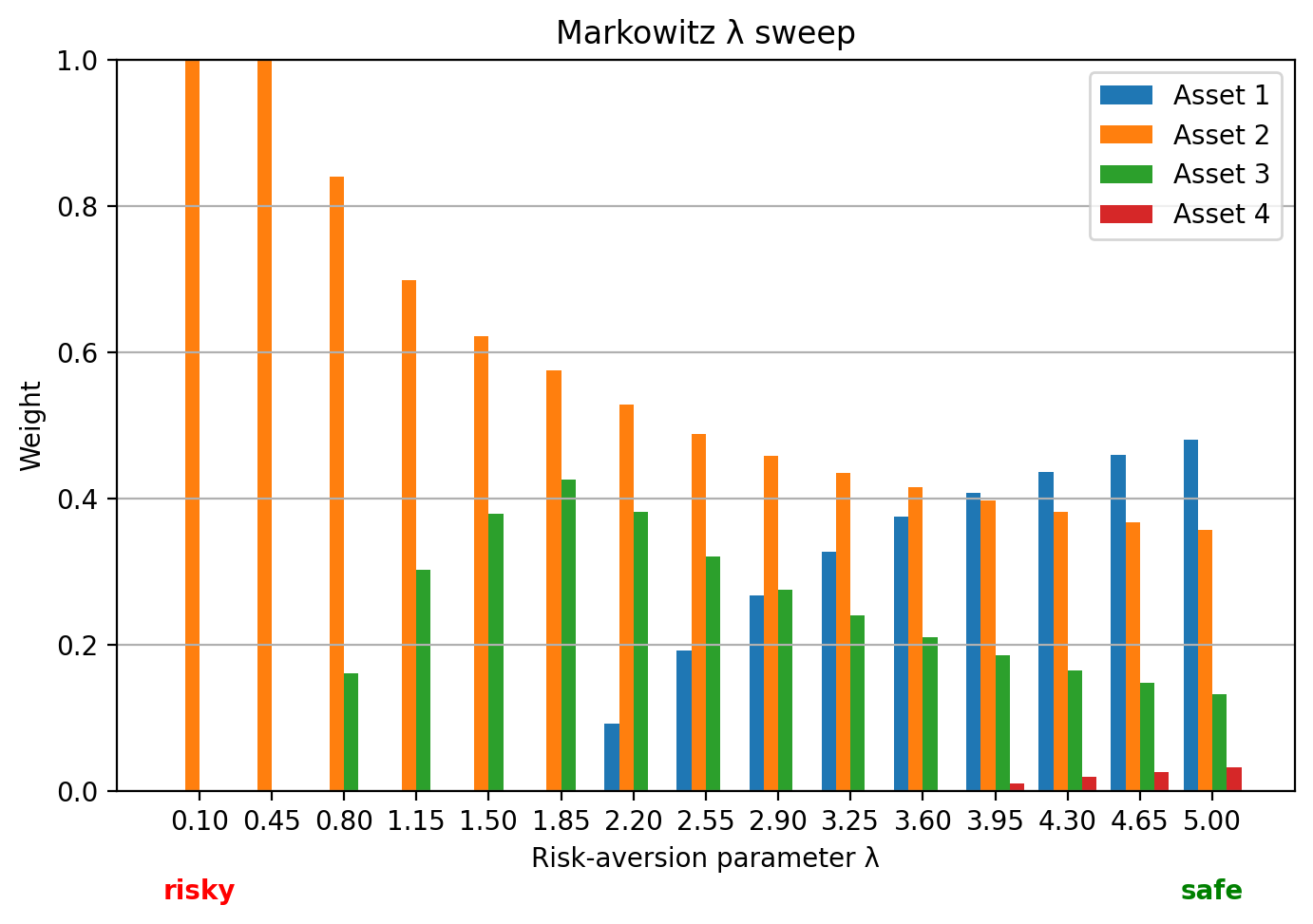

Classical Markowitz Synthetic Figures¶

The classical Markowitz notebook provides reference plots for interpreting quantum portfolio outputs. These plots are useful for checking whether quantum-generated candidates sit in sensible risk-return regions.

Artifact |

What it shows |

|---|---|

Risk-return scatter |

Candidate portfolios colored by return/risk behavior |

Markowitz lambda sweep |

Classical allocation changes across risk-aversion settings |

Real-Data Results¶

Real-data notebooks use market data for a fixed 2024-01-01 to 2025-01-01 window. The committed values below come from notebook output cells and should be regenerated whenever the real-data notebooks are rerun.

Real-Data Summary¶

Dataset |

Method |

Type |

Window |

Selection or frontier |

Return |

Risk |

Objective |

Feasible |

|---|---|---|---|---|---|---|---|---|

Real binary example |

Binary VQE Top-K |

Quantum |

2024-01-01 to 2025-01-01 |

NVDA, AMZN |

0.681501 |

0.335301 |

not printed |

yes |

Real binary example |

Classical equal-weight evaluation |

Classical evaluation |

2024-01-01 to 2025-01-01 |

NVDA, AMZN |

0.681501 |

0.335301 |

not printed |

yes |

Real QAOA example |

QAOA X best feasible |

Quantum |

2024-01-01 to 2025-01-01 |

AAPL, NVDA |

not printed |

not printed |

-0.205323 |

yes |

Real QAOA example |

QAOA XY best feasible |

Quantum |

2024-01-01 to 2025-01-01 |

AAPL, NVDA |

not printed |

not printed |

-0.205323 |

yes |

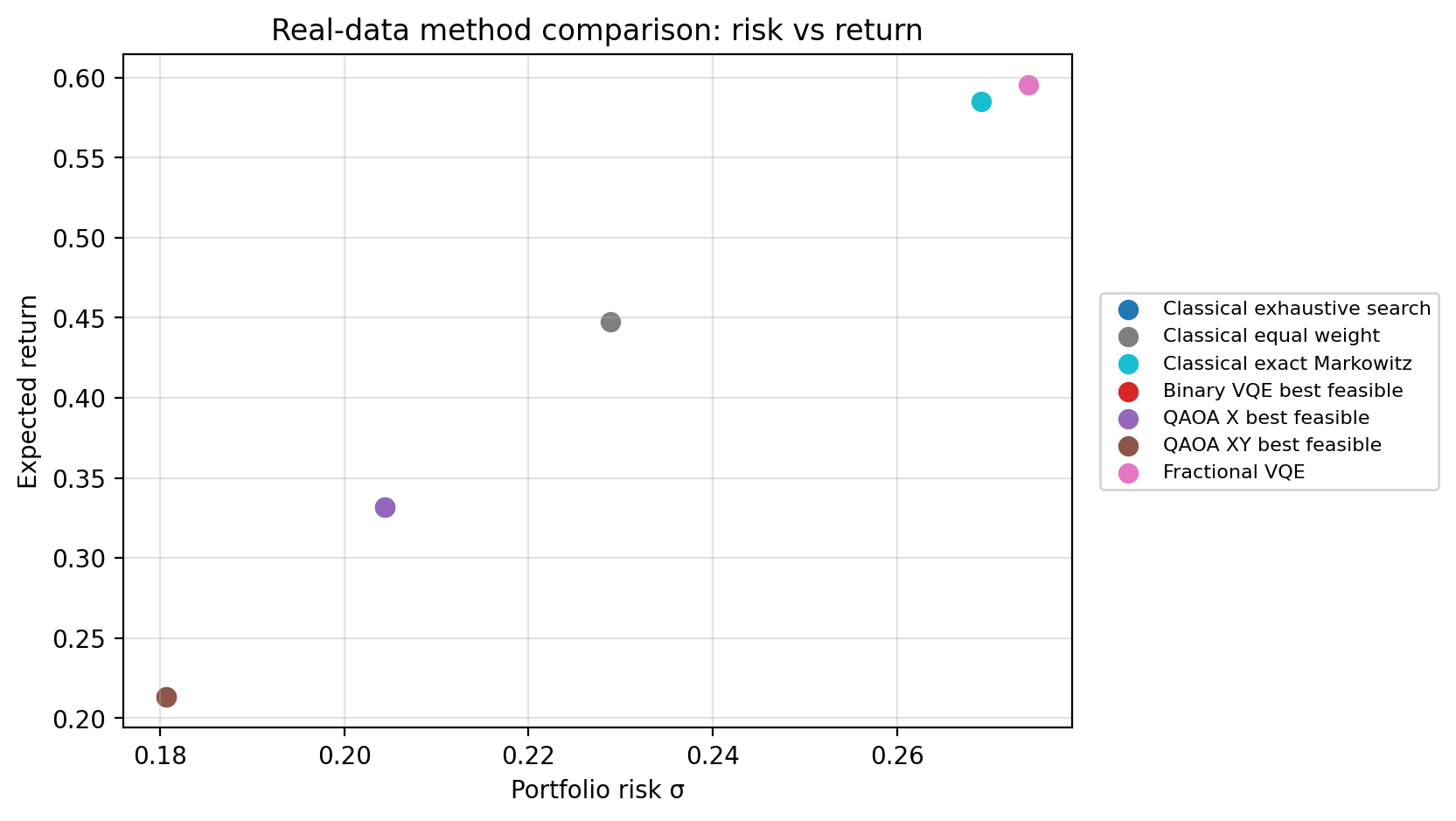

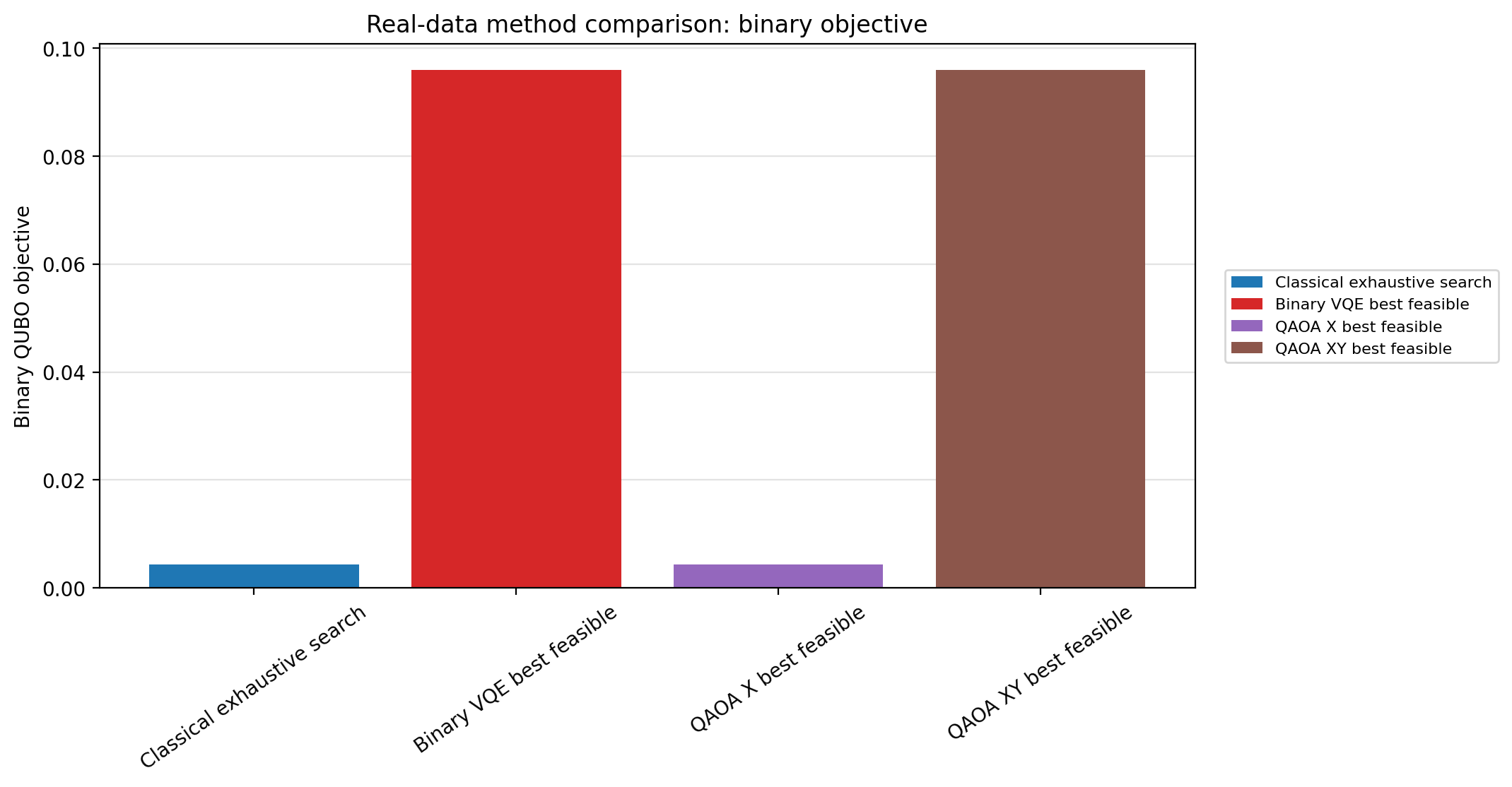

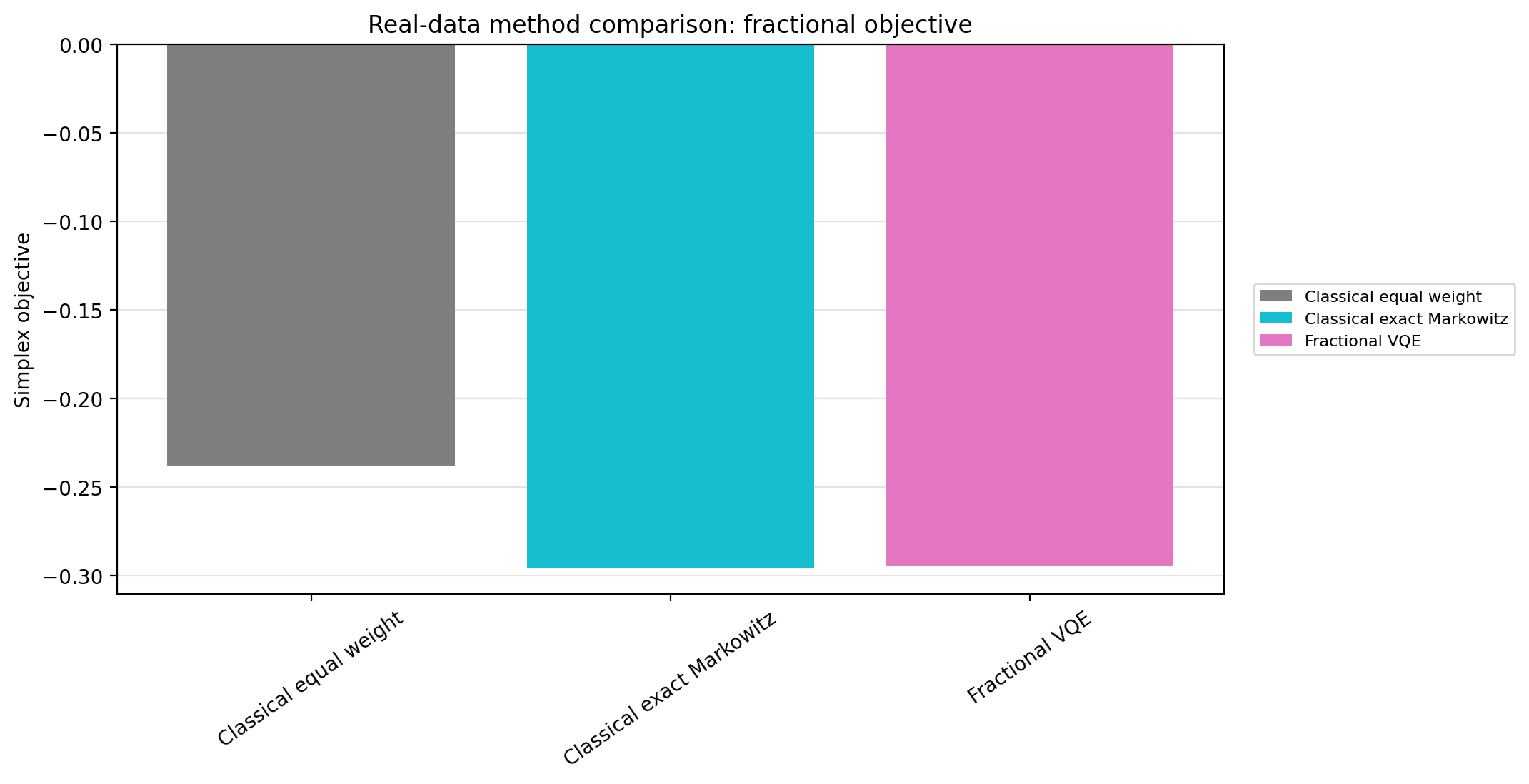

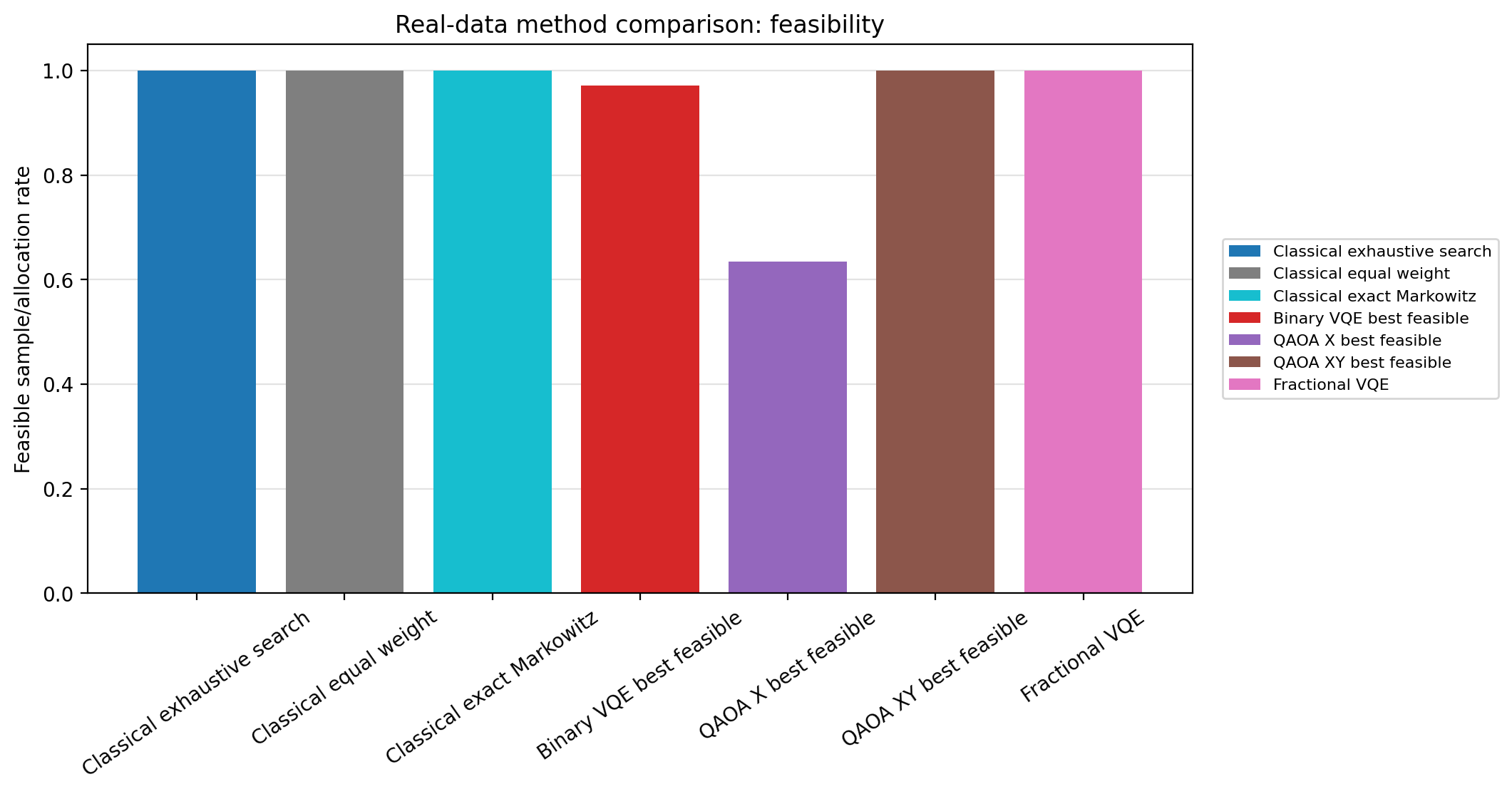

Real-Data Method Comparison¶

notebooks/Real_Data_Comparison.ipynb writes results/real_data_method_comparison.csv and plots the same-method comparison from those rows.

Binary rows use equal-weight selected portfolios for reported return and risk, while objective values remain true binary QUBO objectives. Fractional rows use simplex weights and simplex objectives.

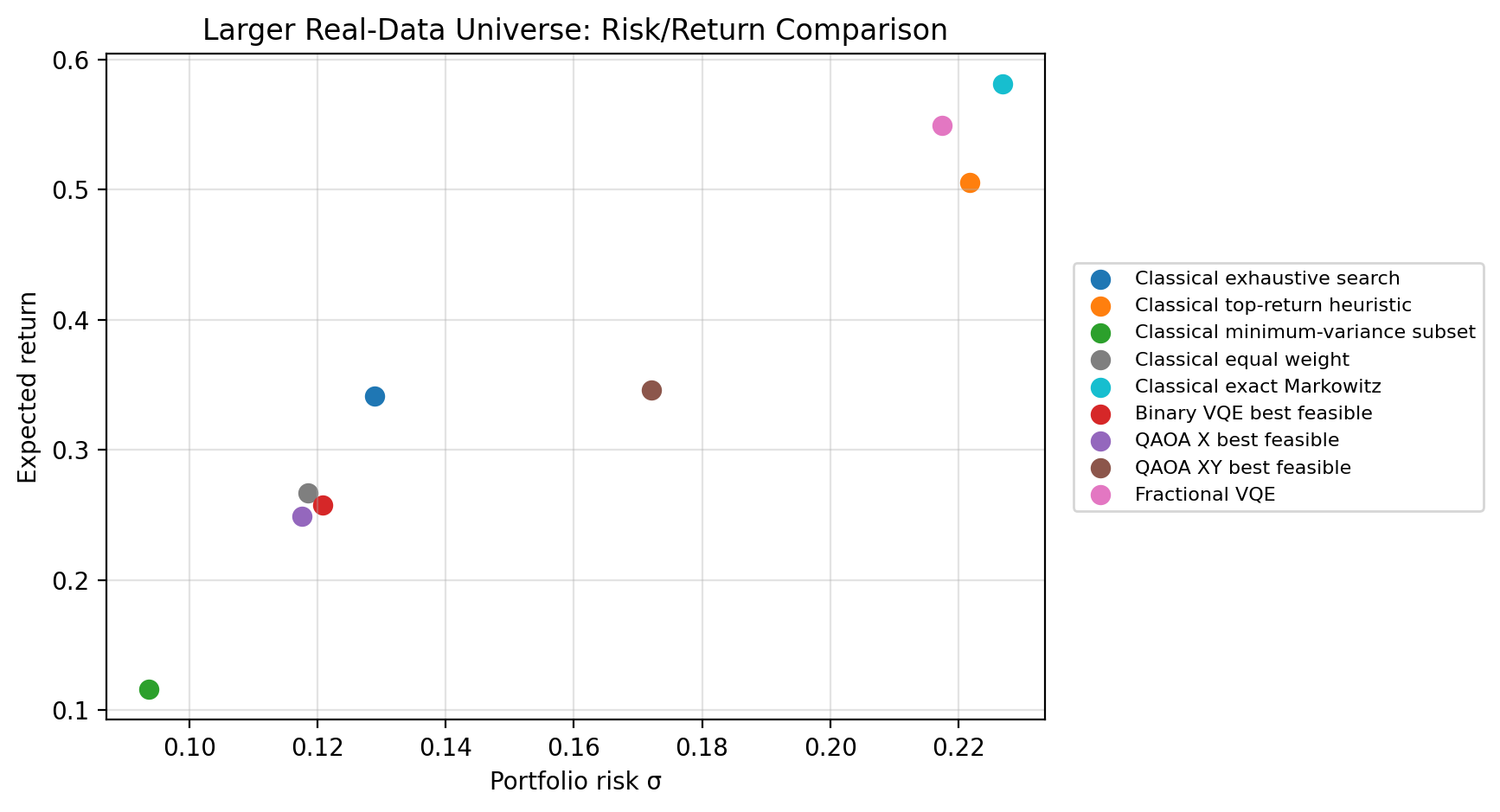

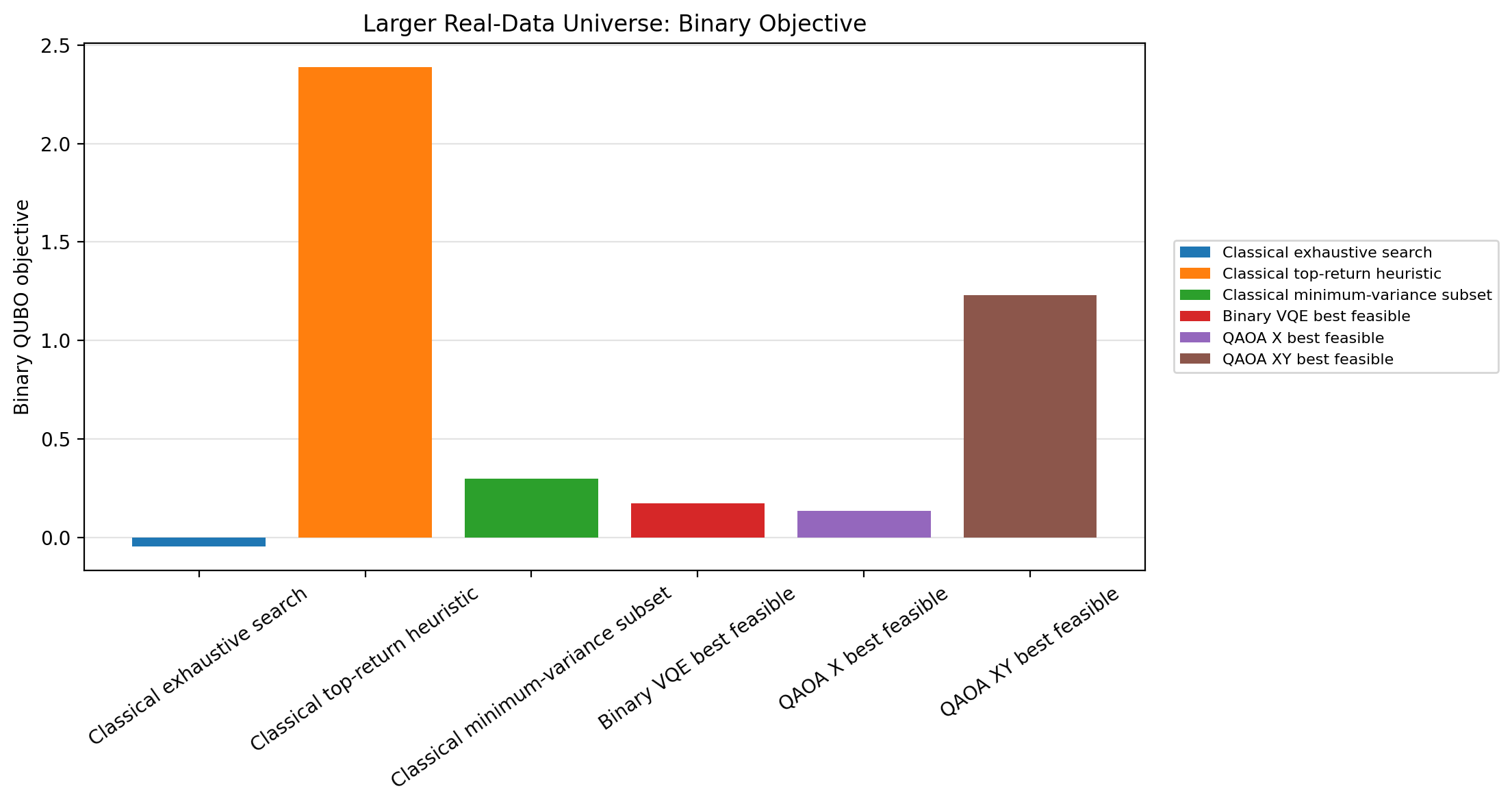

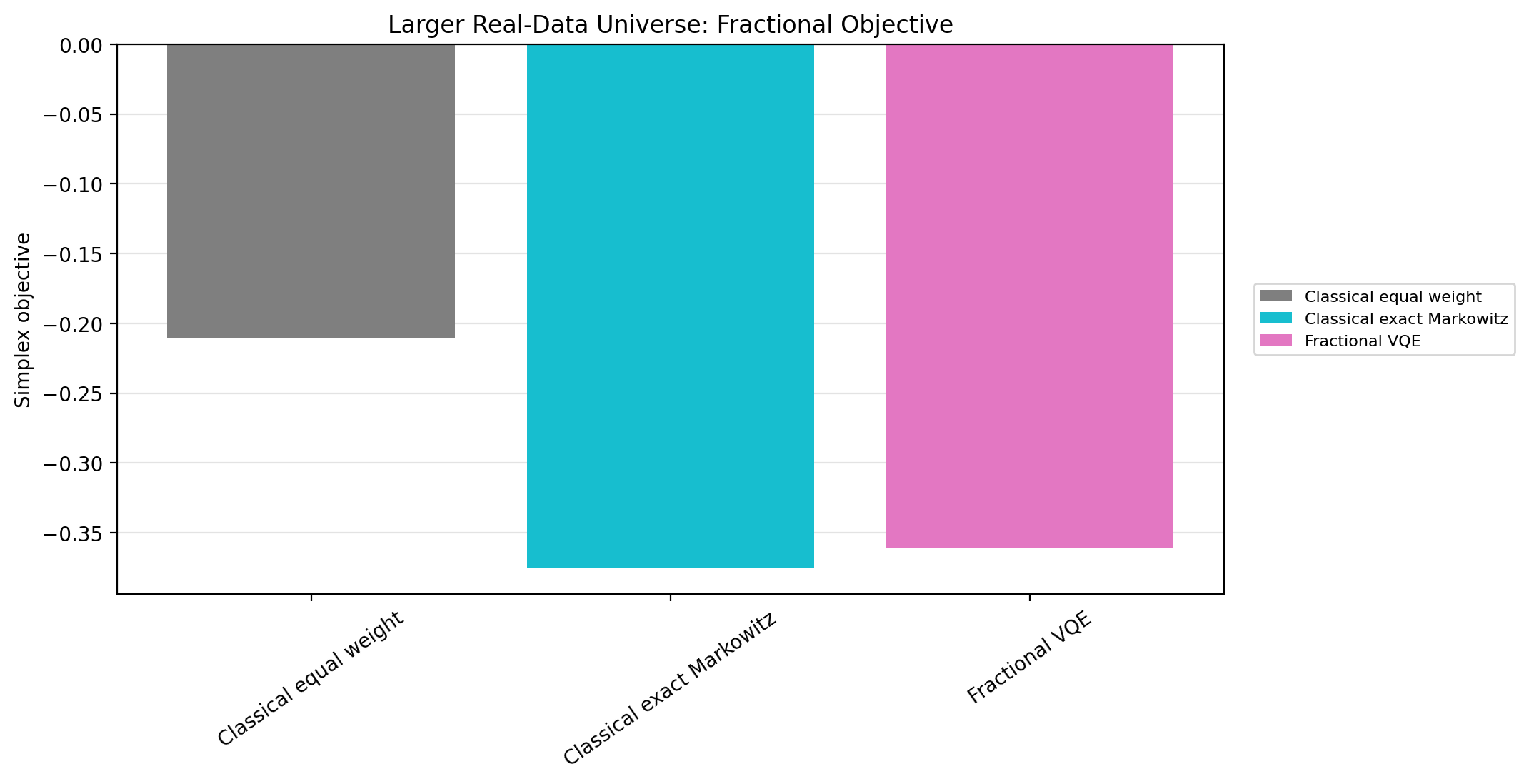

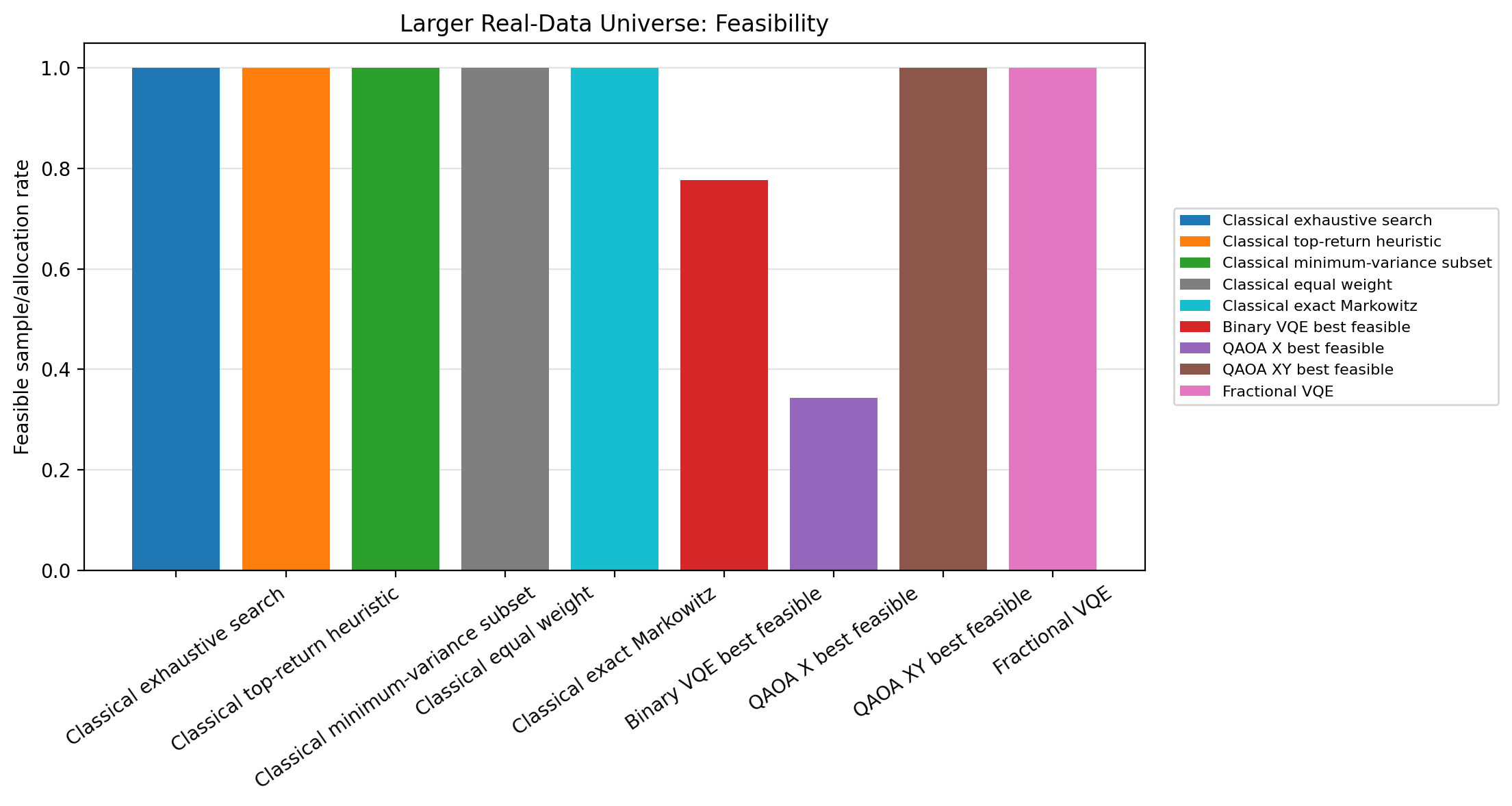

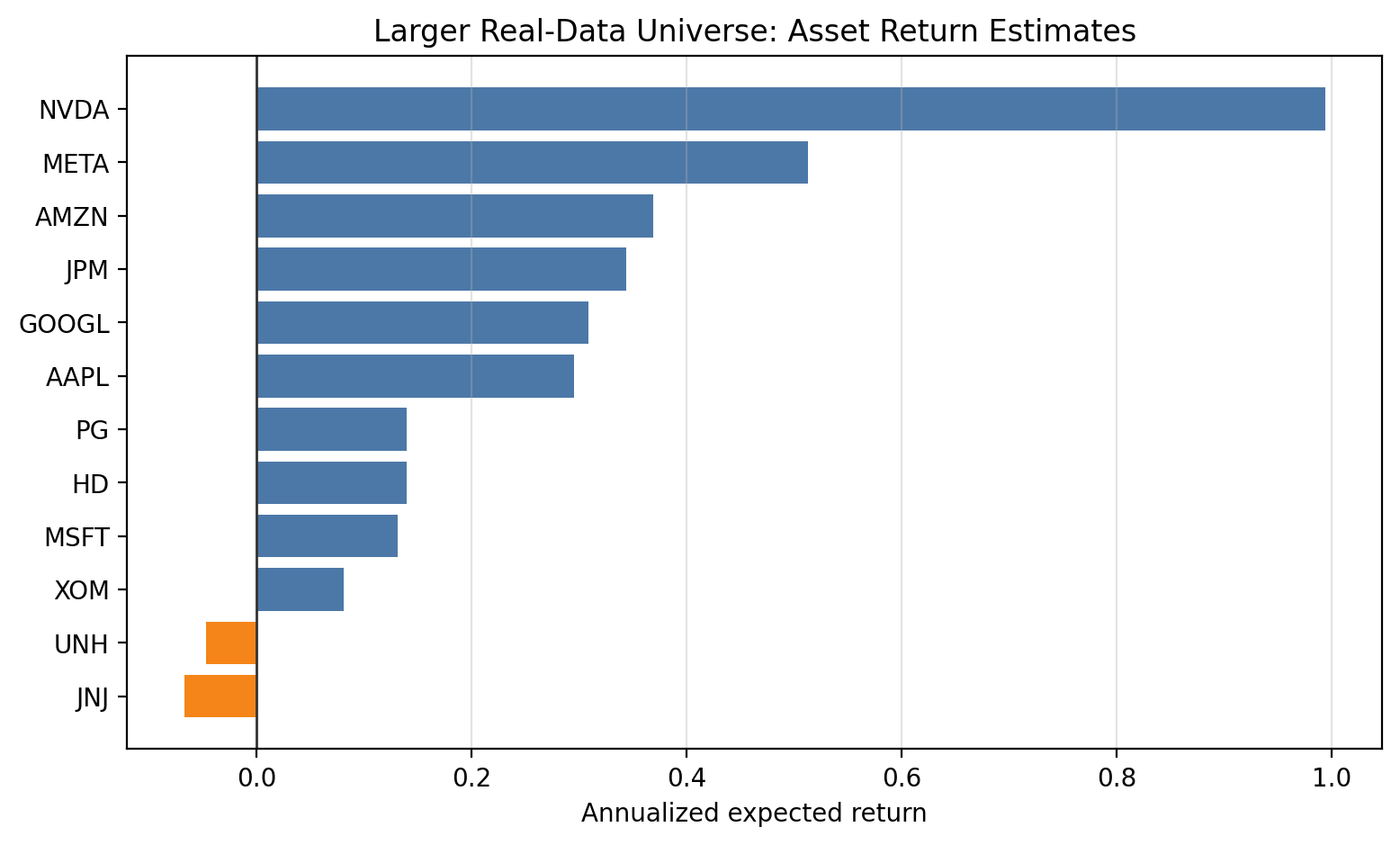

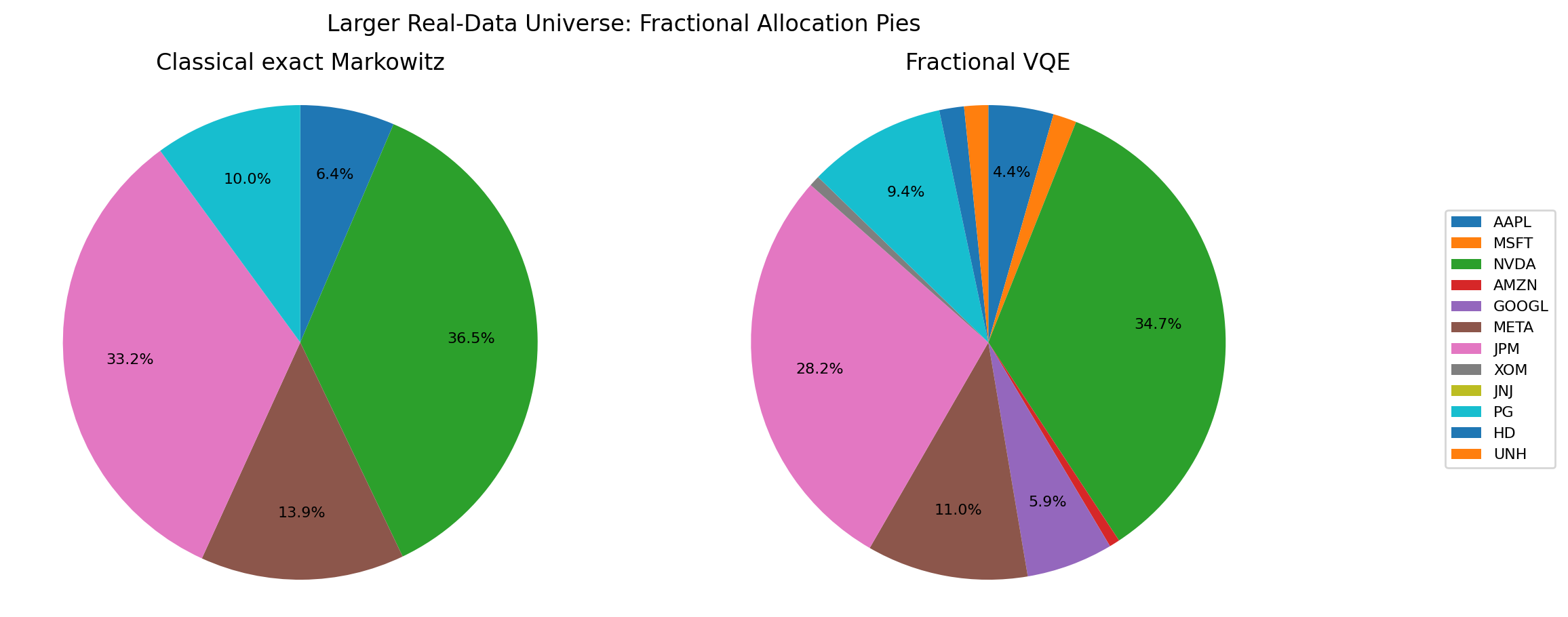

Larger Real-Data Universe¶

scripts/generate_larger_real_data_example.py writes results/larger_real_data_comparison.csv, regenerates notebooks/examples/04_Larger_Real_Data_Example.ipynb, and saves figures for a 12-stock 2024 market-data window. The binary and QAOA methods use one qubit per asset, so this example is deliberately a scalability/stress example rather than a claim of production scale or quantum advantage.

Regenerate it with:

python scripts/generate_larger_real_data_example.py

Method |

Objective family |

K |

Selection or weights |

Return |

Risk |

Best objective |

Feasible rate |

|---|---|---|---|---|---|---|---|

Classical exhaustive search |

binary QUBO |

5 |

AAPL, NVDA, JPM, JNJ, PG |

0.341060 |

0.128919 |

-0.043287 |

1.000000 |

Binary VQE best feasible |

binary QUBO |

5 |

NVDA, XOM, JNJ, PG, HD |

0.257295 |

0.120824 |

0.173363 |

0.777344 |

QAOA X best feasible |

binary QUBO |

5 |

AAPL, META, JPM, PG, UNH |

0.248903 |

0.117525 |

0.136708 |

0.343750 |

QAOA XY best feasible |

binary QUBO |

5 |

MSFT, NVDA, GOOGL, JPM, UNH |

0.346208 |

0.172098 |

1.230733 |

1.000000 |

Classical exact Markowitz |

fractional simplex |

simplex weights |

0.580921 |

0.226857 |

-0.375066 |

1.000000 |

|

Fractional VQE |

fractional simplex |

simplex weights |

0.549605 |

0.217478 |

-0.360419 |

1.000000 |

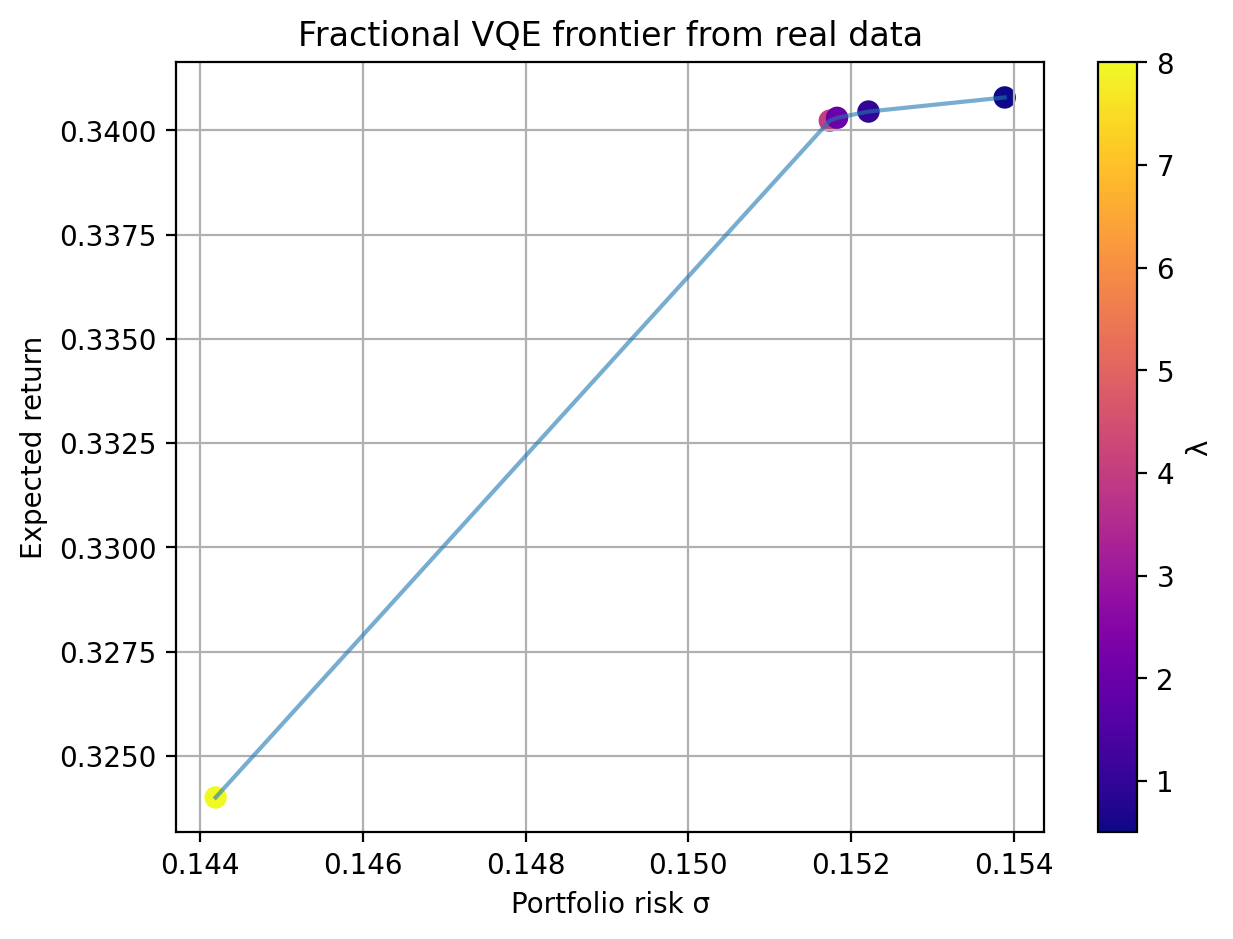

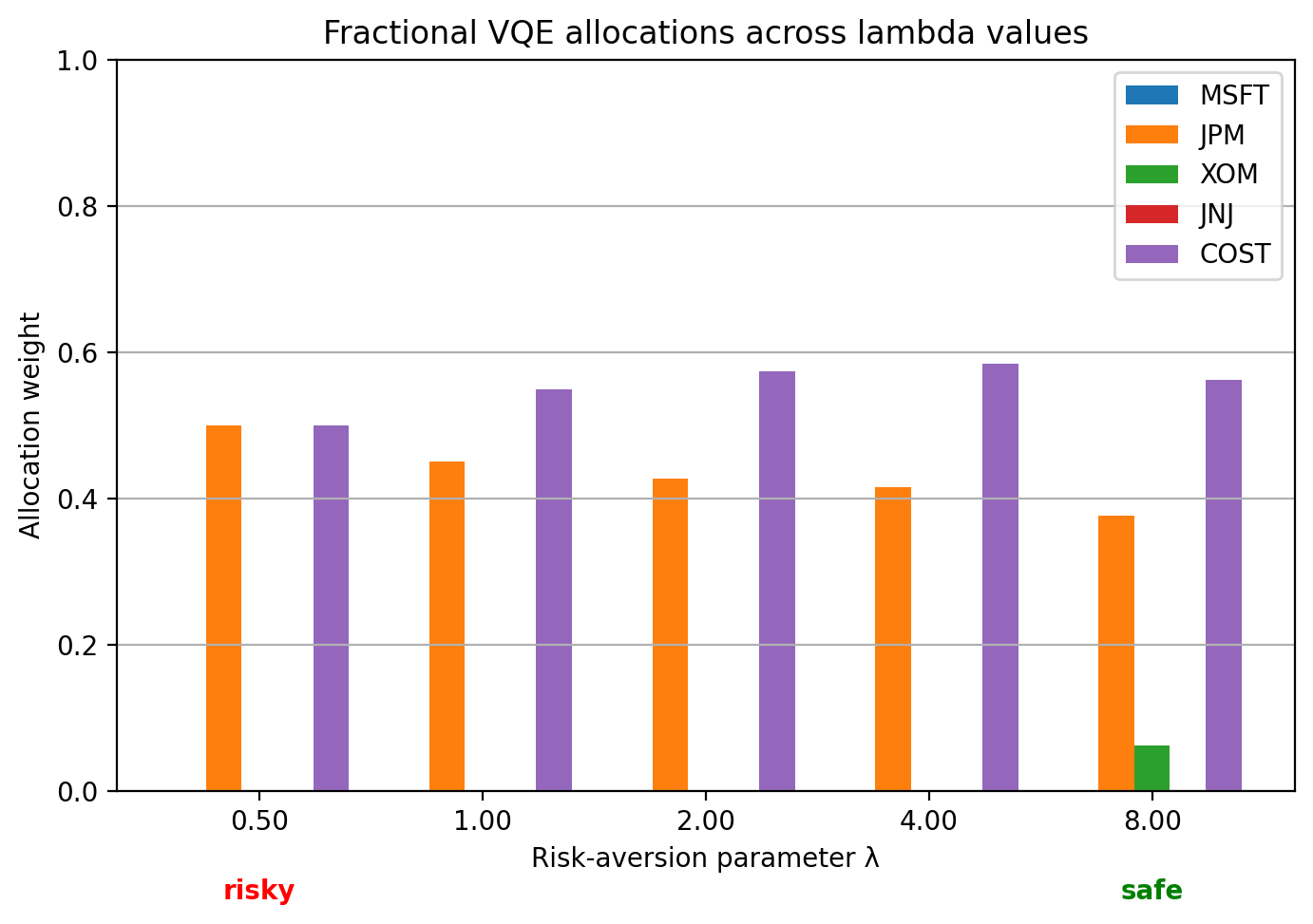

Real Fractional Frontier¶

Method |

λ |

Return |

Risk |

|---|---|---|---|

Fractional VQE |

8.00 |

0.324008 |

0.144192 |

Fractional VQE |

4.00 |

0.340232 |

0.151739 |

Fractional VQE |

2.00 |

0.340300 |

0.151828 |

Fractional VQE |

1.00 |

0.340450 |

0.152215 |

Fractional VQE |

0.50 |

0.340788 |

0.153889 |

Real Binary VQE Figures¶

Example |

Workflow |

Figures |

|---|---|---|

|

Binary VQE |

Convergence, probabilities, Top-K selection |

Real QAOA Figures¶

Example |

Workflow |

Figures |

|---|---|---|

|

QAOA |

Mixer comparison, probabilities, Top-K selections |

Real Fractional VQE Figures¶

Example |

Workflow |

Figures |

|---|---|---|

|

Fractional VQE |

Allocation, frontier, lambda sweep, convergence |

Reproducing These Figures¶

Run the notebooks from the repository root after installing the relevant extras:

pip install -e ".[all]"

Then open the notebook clients:

notebooks/Binary.ipynbnotebooks/QAOA.ipynbnotebooks/Fractional.ipynbnotebooks/Benchmark_Comparison.ipynbnotebooks/Real_Data_Comparison.ipynbnotebooks/Ansatz_Comparison.ipynbnotebooks/Classical_Markowitz.ipynbnotebooks/examples/01_Real_example.ipynbnotebooks/examples/02_Real_Example.ipynbnotebooks/examples/03_Real_Example.ipynbnotebooks/examples/04_Larger_Real_Data_Example.ipynb

The notebooks should save updated plots under notebooks/images/ and notebooks/examples/images/.